IMAGE CREDITS- ONGC, HAZIRA.

IMAGE CREDITS- ONGC, HAZIRA.Until the mid-twentieth century, natural gas was mostly treated as a by-product of crude oil and “flared” (burned as a waste product) during the recovery of the latter.[1] Restricted to meeting the lighting needs of the local community, it only gained prominence after the viability of its transport over long distances and its subsequent storage was established. Moreover, although it was a better alternative to coal, natural gas was initially sidelined by inexpensive crude oil supplies from West Asia to meet the heating and lighting needs of the developed economies of North America, Europe, and East Asia. However, supply vulnerabilities and surging prices, arising out of the oil shock of 1973, exposed the risks associated with excessive reliance on any single source of energy to meet domestic requirements. In response, governments began to introduce different sources of energy, including fossil- and non-fossil fuels, into the economy to meet domestic energy requirements.

Success in the efforts to diversify the primary energy mix of a country relies on the latter’s ability to integrate the “4 A’s of energy security” (that is, availability, accessibility, affordability, and acceptability).[2] Thanks to its relatively wide geographical distribution, the imports of natural gas are perceived to be less vulnerable to geopolitical and geo-economic risks. This perception is particularly strong when comparing the source regions of natural gas with those of crude oil. The source regions of the latter are far more geographically limited and, within the Indo-Pacific, tend to be concentrated in geopolitically sensitive or turbulent sub-regions such as West Asia in general and the Persian Gulf in particular. Additionally, natural gas supplies from non-conventional sources, such as shale gas from the United States of America (USA), and also new discoveries, have dampened the high prices that were earlier (right up to the last decade) associated with natural gas.[3] Natural gas burns more cleanly than does coal or petroleum, it emits less sulphur, carbon, and nitrogen compounds, and also releases far less particulate matter (ash and soot) into the atmosphere.[4] This last feature of natural gas has contributed to its widespread acceptance as an “environmentally friendly fossil fuel” that could, at the very least, “bridge” the gaps associated with renewable forms of energy.[5] In recent times, these features of natural gas have led to its being seen to be the fastest-growing fossil fuel in the world.[6] Increased global demand has thus far been led by China, which is attempting to combat severe air pollution in its cities by gradually replacing coal with natural gas in the heating and lighting and industrial sectors.[7]

India, too, has sought to capitalise upon the relative “cleanliness” of natural gas, despite it being a fossil fuel. However, while the preference for natural gas is a consistent feature over the past two decades, there has been a very significant shifting of “goalposts” that is discernible over time, on the one hand, and also across the capstone policy documents published by the concerned departments/agencies of the government, on the other. An undue reliance upon merely the “latest” articulation by a given department of the government without cross-referencing it to other earlier documents leads to a loss of credibility of the data itself. For example, the India Hydrocarbon Vision-2025, which was presented in the year 2000, had, of course, promoted the “use of natural gas, which is relatively a clean fuel” and had acknowledged the need to supplement domestic sources with imports of Liquefied Natural Gas (LNG).[8] More importantly, however, it estimated that 20 per cent of India’s primary energy mix would comprise natural gas by 2025. Just six years down the line (in the year 2006), the Integrated Energy Policy projected that the share of natural gas would be 11 per cent by 2032.[9] In other words, it halved the estimation of percentage share (from 20 per cent to 11 per cent), even as it increased the time (from the year 2025 to the year 2032) over which this sharply reduced target would be achieved. A further seven years later (in May 2013), one finds a third document, this one promulgated by the regulator of India’s downstream (refining and distribution) sector, namely the Petroleum & Natural Gas Regulatory Board (PNGRB). This document — “Vision 2030”: Natural Gas Infrastructure in India — ramped up the percentage share being targeted in respect of natural gas (from 11 per cent to 15 per cent) and reduced the time (from the year 2032 to the year 2030).[10] In the absence of any correlative or explanatory notes to justify these shifts of percentage-share targets and the time frame over which they are sought to be achieved, both monitoring and analysis tend to flounder.

It could be reasonably concluded that India tempered the optimism of the estimates promulgated via the India Hydrocarbon Vision-2025 when it was forced to confront the reality that massive reforms in the industry were a precondition for this sort of expansion of the share of natural gas in the primary energy mix of the country. This might suffice to explain the first shifting of goalposts. However, if the second shift, increasing the percentage share and reducing the time frame, is to be afforded credibility, it would imply that these massive reforms and the concomitant development of infrastructure have been completed or are proceeding ahead of the estimations and faster than expected. Is this, in fact, the case?

As has already been stated, what has remained consistent is the country’s commitment to natural gas, at least as a “bridging” strategy. In his inaugural address to the representatives of the global oil and gas industry at the Fourth India Energy Forum on 26 October 2020, Prime Minister Narendra Modi affirmed India’s commitment to “shift to a gas-based economy”.[11] This policy would encompass:

- An expansion of present efforts to develop indigenous sources of natural gas.

- The attainment of a dedicated and unified natural gas transmission network under the “One Nation One Gas Grid” policy.

- The implementation of Natural Gas Marketing Reforms to achieve a market price discovery of gas.

The first amongst seven other components of India’s energy strategy for the future, the shift to a gas-based economy, eclipsed even the highly advertised expansion of the country’s renewable energy target from 175 gigawatts (GW) by 2022 to 450 GW by 2030. By stressing the need to develop domestic sources of natural gas, Prime Minister Modi has linked this feature of the new policy with the broader goal of achieving a 10 per cent reduction in (oil) imports by 2022. At the same time, this support for domestic sources of natural gas (and their exploitation by Indian entities) will form an integral element of the year-old Atmanirbhar Bharat (Self-reliant India) vision of indigenisation.[12]

The latest reiteration of an objective that has so far evaded three governments at the national level since 2000, the revised target is backed by a value chain that has matured over the past two decades. For instance, in 2000, India had no capacity to absorb LNG, and its Exploration and Production (E&P) efforts were limited to shallow depths. Today, more than half of India’s gas consumption comprises LNG imports, and it can tap gas reserves trapped in reservoirs up to 3,000 metres below sea level. Hence, the shifting goalposts (targets) notwithstanding, India is in an advantageous position to attain its revised target. However, the country still faces an uphill battle to increase the share of natural gas in the economy. Envisaging a target audience comprising policymakers in India’s energy sector, this article examines some internal challenges to India’s objective of establishing a gas-based economy. Changing consumption patterns, which will determine the share of LNG imports, and infrastructure deficits, are vital to this study since these will influence India’s capacity to absorb augmented supplies of natural gas, irrespective of its source. The article also underscores concerns arising from ongoing and future competition with other fossil- and non-fossil fuels. In continuation of the National Maritime Foundation’s research studies on the maritime facets of India’s energy security, the article will also assess the geopolitical implications of India’s strategy.

ASSESSING THE INDIAN CONTEXT

Supply of Natural Gas to the Indian Economy

Unlike the industrialised nations of Europe, North America, and East Asia, the consumption of natural gas in the Indian economy was very low, largely due to the limited available domestic supply, sourced mainly from gas fields in the country’s North East. Only with the discovery of huge gas reserves off the west coast of India in the 1970s did the consumption of natural gas escalate.[13] Since climate change was not a priority for most governments and the flexibility to meet sudden spikes in power demand, known as “ramp-up capacity”, was met primarily by large hydropower, the limited volumes of available domestic supply of natural gas were committed to the manufacturing sector. In short, these reserves were still inadequate to challenge the dominance of coal in power generation or crude oil in transportation. Later, however, the steadily rising demand for electricity compelled the Government of India (GoI) to divert natural gas supplies mainly to power generation and fertiliser production. This remained the case throughout the 1990s.[14]

Meanwhile, India’s Public Sector Undertakings (PSUs), led by the Oil and Natural Gas Corporation (ONGC) and Oil India Limited (OIL), which hitherto had led India’s exploration efforts, gradually began making way for private players, such as Reliance, British Petroleum (United Kingdom), ENI (Italy), and Cairn Energy (United Kingdom), under the erstwhile New Exploration Licensing Policy (NELP). The NELP, a profit-sharing regime that opened up E&P to private and foreign players, encouraged Foreign Direct Investment (FDI) up to 100 per cent in E&P efforts. For the first time since Independence, this policy created a level playing field for all investors, which rejuvenated India’s efforts to augment falling domestic petroleum and natural reserves.

The discovery of fresh domestic sources of natural gas — from reserves off India’s east coast in October 2002 — led to another boom in terms of its adoption as a fuel for power generation (amongst other sectoral utilisation), in increasingly popular combined-cycle power plants. Moreover, its emergent consumption in the transportation sector — in the form of Compressed Natural Gas (CNG) — and as a household cooking fuel — by way of Piped Natural Gas (PNG) — strengthened the demand for a substitute to diesel/petrol, coal, and firewood, with a fuel that had very low particulate matter (PM).[15] So intense was the demand for an indigenous source of energy that Reliance Industries Limited (RIL), the lead investor in the KG-D6 (Krishna Godavari Dhirubhai 6) exploration block (See Figure 1), began large-scale commercial production in 2009 — a record six and a half years after initial discovery.[16]

Figure 1: LNG Infrastructure in India Source: Created by the author with data from the Corporate Profile of Petronet LNG Limited https://www.petronetlng.com/PDF/CorporatePresentation.pdf, and HEnergy http://www.henergy.com/project/natural-gas-pipeline-map-of-india/; map sourced from www.d-maps.com *All figures in million metric tonnes per annum [MMTPA] **FSRU: Floating storage and regasification unit ***The former state of Jammu and Kashmir (J&K) was reorganised into a Union Territory and bifurcated into the Jammu and Kashmir Union Territory and the Ladakh Union Territory in August 2019. |

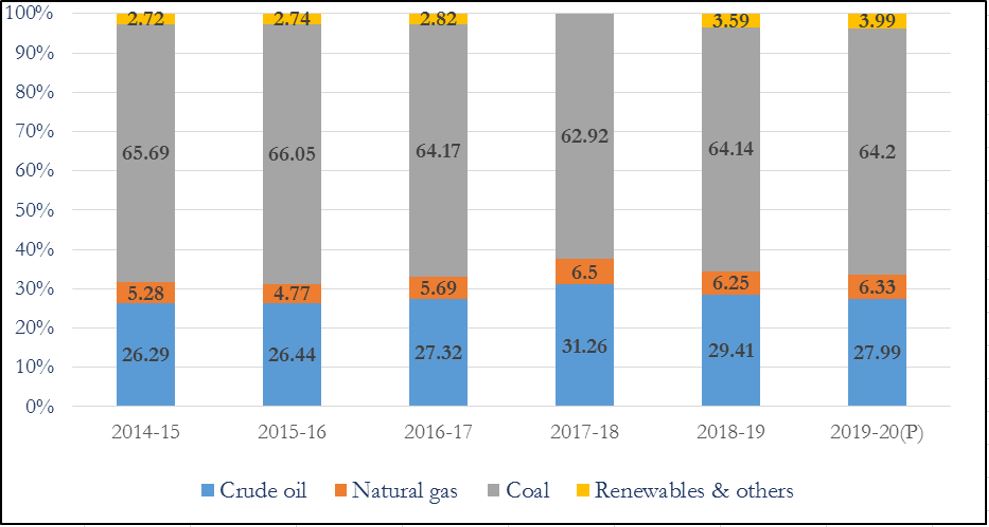

However, even after the latest boom phase in its popular adoption, natural gas’s share of the total primary energy supply (TPES) — a key indicator of India’s fuel mix — amounted to only 6.33 per cent in 2019–20.[17] In fact, in recent years, natural gas has never amounted to more than seven per cent of India’s fuel mix (see Figure 2), while the global average was 23.71 per cent in 2019.[18]

Figure 2: Fuel Shares in Total Primary Energy Supply Source: Compiled by author with data from Energy Statistics 2016–21, National Statistical Office, Ministry of Statistics and Programme Implementation, Government of India. |

Exploration and Production (E&P) Activities

Geological complexities of deep-water production, a massive overestimation of available reserves, compounded by contractual disruptions, were largely responsible for the tremendous decline of output from KG-D6, which also contributed to the overall shrinkage of natural gas supply from domestic production.[19] Figure 3 draws attention to the diminishing production of natural gas within India since 2010. It also shows that even though domestic sources contributed a larger portion of the available supply, the net imports have been steadily rising.

Preliminary data from 2019–20 shows that LNG imports now comprise more than half the total supply, and this trend may continue if domestic production stagnates. Thus, as the demand for this low-carbon fuel grows, any failure to supply adequate volumes of this “in-demand” commodity from domestic sources will not only lead to a greater dependence on LNG imports to fill the vacuum but also necessitate the expenditure of considerable political and economic resources to access stable sources of supply.

The falling domestic production of a resource is a worry for any government attempting to balance the trade deficit. In the Fiscal Year (FY) 2019–20, India imported approximately US$ 8.9 billion of LNG.[20] Combined with crude oil (US$ 101.38 billion), oil and gas imports form the largest share of commodities imported by India.[21] Given India’s status as a developing country, it is fairly obvious that energy demand will continue to grow. However, unrestrained energy imports could devalue the rupee and have a negative spillover into other sectors like education, health, defence, and so forth. While it is certain that India cannot achieve the broader 10 per cent reduction in oil imports by 2022, the expansion of its effort to develop indigenous sources of natural gas signals the government’s commitment to bolster energy security by reducing its dependence on expensive LNG imports.

Figure 3: Availability of Natural Gas in India (billion cubic metres) Source: Compiled by author with data from Energy Statistics 2021, National Statistical Office, Ministry of Statistics and Programme Implementation, Government of India, 52. |

Pricing of LNG Imports and Domestic Natural Gas Supplies

Since 2014, the price of natural gas extracted from domestic sources has been pegged with the existing prices from sources in the USA, Mexico, Canada, the European Union, and Russia. This price is less expensive than what producers in India would gain if their product was pegged to the Japan–Korea Marker for LNG, which prevails in the East Asian market. Natural gas prices from domestic sources are reviewed every six months, and are based on the past year’s price and volume of supply. Conversely, supplies imported as a result of India’s long-term LNG contracts are linked to the global crude oil price.

At present, domestically produced natural gas — priced at US$ 3.62/MMBTU (Metric Million British Thermal Unit) — and imported r-LNG (re-gasified Liquefied Natural Gas) — priced at an average US$ 2.68/MMBTU in the spot market and an average US$ 9–10/MMBTU according to the long-term contract with Qatar — are the only two modes of natural gas supply in India.[22] Although the price differential between spot cargoes and long-term contracts is stark, the fluidity of the former, especially when the demand for heating increases in the northern hemisphere, is a deterrent to the expansion of LNG imports to India. For instance, the average price of spot cargoes was close to US$ 18/MMBTU in January 2021.[23] Such a huge spike in the average price of LNG led to the shaving of demand from India in FY 2020–21, estimated at 1.8 Million Metric Tonnes (MMT) [2.44 BCM] in January 2021, from a peak of 2.5 MMT [3.40 BCM] in October 2020.[24] Such a sensitivity to global demand will have to be tempered by an expansion of indigenous production and the development of economies of scale in India.

Gas Infrastructure

There are two options available for the import of natural gas into India. The geographical proximity to the gas-rich West (Iran), Central (Turkmenistan), and Southeast (Myanmar) Asian regions stimulated a decades-long discussion for the establishment of cross-border and undersea gas pipeline networks. However, geopolitical rivalries with Pakistan and China and India’s inability to circumvent the US embargo on Iranian energy supplies, as well as the prohibitive costs of international pipelines, have frustrated any attempts to move beyond initial discussions.[25] This leaves LNG imports as the only viable alternative. With the capacity to process 42.5 million metric tonnes per annum (MMTPA) of natural gas (57.8 BCM), India is among the world’s top-five importers of LNG.

An adequate transportation network is the most vital feature of the successful expansion of natural gas consumption.[26] In the case of India, the 17,000 kilometres of inter-state pipeline network, which currently favours developments around the LNG terminals located on the west coast, has been targeted for rapid expansion to facilitate natural gas use in the eastern regions under the “One Nation One Gas Grid” policy (see Figure 1).

An often-overlooked aspect of India’s natural gas infrastructure is the shortfall in state-owned LNG carrier capacity. Presently, the state-owned Shipping Corporation of India (SCI) manages and operates four second-hand joint-venture-owned LNG carriers. In sharp contrast, as of 2019, China owned as many as thirty-eight LNG carriers. The SCI has leased its vessels on long-term time charters to Petronet and Exxon Mobil. In aggregate, these four vessels have a capacity of 604,000 cubic metres (m³).[27] In comparison, the largest LNG carrier in the world can accommodate 266,000 m3 of LNG. The prohibitive costs of purchasing new LNG carriers and the absence of shipbuilding expertise have compelled India to opt for the services of foreign-owned vessels.[28] While this may seem a far less expensive option than purchasing a new LNG tanker, the events of the past few months showcase the volatility of the status quo. In January 2021, LNG spot charter rates touched an all-time high of US$ 300,000 on some routes due to surging demand for LNG supplies in winter.[29] India, which is increasingly purchasing LNG in the spot market, could lose potential cost advantages if the cost of shipping the cargo is excessive.

Domestic Consumption Patterns

Figure 4 shows that of the total natural gas supply in 2018–19, 22.30 per cent fed the 74 gas-fired plants in India.[30] Most of these types of thermal plants employ Combined Cycle Gas Turbine (CCGT) technology to generate electricity. In conjunction with the fertiliser industry (27.8 per cent), these two “anchor customers” of natural gas absorbed 50 per cent of the total available supply in 2018–19.[31] Moreover, along with the City Gas Distribution (CGD) network, power generation and fertiliser production receive priority domestic gas, according to India’s Gas Utilization Policy.[32]

In the case of power generation, gas-fired power plants are far more efficient than other thermal power plants that use coal, lignite, or diesel.[33] In India, the performance of a power plant is gauged on its ability to attain a high Plant Load Factor (PLF). PLF is defined as the “percentage of sent out energy corresponding to installed capacity in that period”.[34] Gas-fired plants employing CCGT technology can attain more than 50 per cent PLF.[35] To understand the link between PLF and gas-fired generation, consider the following example: If the installed capacity of a thermal generation station is 1,000 megawatt (MW), it can produce a maximum of 24,000 megawatt-hour (MWh) of electricity in a 24-hour period [1000 MW x 24 hours = 24,000 MWh]. It is extremely difficult for thermal generation units to achieve and maintain complete utilisation of available capacity. Assuming that a power plant utilised only 800 MW of its installed capacity in one day, the total electricity generated is 19,200 MWh (800 MW x 24 hours). Hence, the PLF of the thermal generation station is 80 per cent (19,200 ÷ 24,000 = 0.8 [80 per cent]).

Despite the obvious technological advantages over other thermal sources of electricity, gas-fired power plants in India have been running on an extremely low PLF since 2011–12. By FY 2017–18, the average PLF of gas-fired power plants in India had touched a low of 24 per cent.[36] The shrinking supply of domestic natural gas from the Krishna–Godavari basin and the inability to purchase expensive LNG imports from the international market left as many as 31 gas-fired plants, with a cumulative installed capacity of 14.30 gigawatt (GW), financially unviable. Shockingly, such rising cases of “stranded assets”, in addition to the shortfall of as much as 70 per cent of the gas allocated to the industry, did not desist the addition of 3.7 GW of capacity, which would make these units fully dependent on LNG imports.[37]

On the other hand, CGD, which covers the supply of PNG and CNG, increased its share of natural gas consumption from 5,598.79 million metric standard cubic metres (MMSCM) in 2011–12 to 9,206 MMSCM in 2018–19 — a massive 64 per cent hike from one sector alone. Thus, the expansion of the PNG network to Tier-II cities and the switch to CNG-fuelled public transport due to urban air-quality concerns could ensure this sector’s appetite for a larger share of India’s natural gas supplies.[38]

Figure 4: Sector-wise Percentage Consumption of Natural Gas for 2018–19 Source: Energy Statistics 2020, National Statistical Office, Ministry of Statistics and Programme Implementation, Government of India, 65. Note: The provisional figures for 2019–20 are available, but are not comprehensive. |

INDIA’S LNG IMPORT STRATEGY

Emulating the diversification strategies of Japan, South Korea, and China, India has expanded its sources of imports from well-established sources in West Asia and Europe to emerging players from North America, Africa, Southeast Asia, and Oceania. Since the early 2000s, the share of LNG imports in India’s energy mix has increased significantly. For instance, at the turn of the century, India imported less than US$ 1 million of LNG, and from just one country — Belgium.[39] Only with the commissioning of the re-gasification terminal at Dahej, Gujarat, in 2004, could India opt to expand LNG imports for its booming economy. The US$ 18 million shipment, which arrived from Qatar that year, was in and of itself emblematic and offered a revelation into future dependencies, especially with West Asia.[40]

Table 1 shows the dominance of LNG imports from Qatar — with which India has signed a 25-year long-term contract till 2028 — almost a decade after the first shipments arrived in India. Effectively, the top five sources of imports alone contributed a whopping 99 per cent of the total imports.

| Country | Quantity (BCM) | Share (in per cent) |

| Qatar | 13.96 | 82.02 |

| Nigeria | 1.83 | 10.8 |

| Egypt | 0.7 | 4.11 |

| Trinidad and Tobago | 0.42 | 2.48 |

| Algeria | 0.02 | 0.12 |

| Others (11) | 0.08 | 0.47 |

| Grand Total | 17.02 | 100 |

|

Table 1: Sources of India’s LNG imports in FY 2011–12 Source: Department of Commerce, Ministry of Commerce & Industry, Government of India, “Export-Import Data Bank”, 2021. |

||

In FY 2019–20, nearly two decades after the arrival of that first shipment from Qatar, India imported US$ 9.66 billion of LNG from as many as 16 countries.[41] Subsequent contractions of imports to US$ 7.06 billion in FY 2020–21 (April–February) due to the impact of the COVID-19 pandemic on domestic demand did not stop India’s drive to diversify its imports.

In the ten-year period from FY 2011–12, India increased the number of LNG sources to eighteen — partaking of the abundance of shale gas supplies from the USA as well as a larger share of natural gas from Australia and the African continent (Nigeria, Angola, Egypt, Cameroon, Equatorial Guinea, and Algeria) (see Table 2). Imports from these six African sources comprised 21.04 per cent of the total LNG imports. At the same time, one cannot ignore the fact that while imports from Qatar have halved over a decade, supplies from West Asia — due to upgrades in gas liquefaction and storage facilities in the United Arab Emirates (UAE) and Oman — contributed more than 55 per cent of India’s total LNG imports.[42] Besides Qatar, India has also signed long-term LNG contracts with Australia, Russia, and the USA.

| Country | Quantity (BCM) | Share (in per cent) |

| Qatar | 12.34 | 40.07 |

| United Arab Emirates | 3.86 | 12.55 |

| United States of America | 3.74 | 12.14 |

| Nigeria | 2.74 | 8.89 |

| Angola | 2.42 | 7.85 |

| Others (13) | 5.69 | 18.50 |

| Grand Total | 30.79 | 100 |

|

Table 2: Sources of India’s LNG imports in FY 2020–21 (Apr.–Feb.) Source: Department of Commerce, Ministry of Commerce & Industry, Government of India, “Export-Import Data Bank”, 2021. |

||

Geopolitical Implications of India’s Energy Strategy

The success of India’s diversification strategy can be gauged from the increasing availability of LNG imports in the energy basket. With the commissioning of the LNG terminal at Ennore and the East–West pipeline connecting Hazira to Kakinada, natural gas from Asia and Africa can reach the supply-starved power stations on India’s east coast. A 2018 study by the International Energy Agency (IEA) that examined the abilities of LNG suppliers to overcome demand shocks or supply interruptions classified India as a “diversified gas importer” (with considerable indigenous production) that is moving to become a “diversified LNG importer” (dominated by LNG imports).[43]

The recent spat with Saudi Arabia over the obstinacy of the Organization of the Petroleum Exporting Countries and its allies (OPEC+) to adhere to pre-determined production cuts exposed India’s soft underbelly — oil-import dependency, primarily on West Asian producers. Feeble efforts to diversify away from Saudi Arabian supplies were limited to purchases from the USA and Africa. In the case of LNG, India has reduced its dependence on Qatari imports by increasing its reliance on American imports. However, inadequate reserves of shale and the burgeoning demand from American consumers will be a cause of concern for Indian policymakers. Furthermore, the US administration, under the leadership of President Joe Biden, may curtail shale gas production in favour of accentuating climate-change mitigation policies.[44] A reversal of US policy may compel a return to traditional suppliers with production and export capacities that are resilient to political change.

Over the past decade, India has undertaken several risky investments in geopolitically sensitive countries to access alternative sources of supply. India’s US$ 6.5 billion investment for a 30 per cent stake in the Rovuma gas field in Mozambique remains stuck due to the prolonged political and security challenges arising from the Islamic State-led insurgency in the northern part of the country.[45] Similarly, India’s US$ 400 million play to develop the ONGC-discovered Farzan-B offshore gas field could not disentangle itself from the threat of repercussions of challenging the US-led sanctions on Iran’s energy exports.

Finally, strong political commitment to develop alternate and indigenous energy sources may trigger misgivings among energy suppliers who are focussed on preserving their markets by cultivating their security of demand. For instance, Qatar reduced the price of its LNG supplies to India in 2015 only after India agreed to absorb additional volumes of the commodity. Similarly, the USA’s development of indigenous shale reserves led to the recalibration of West Asian exports to North America and Europe in favour of the Indo-Pacific region, where countries like India and China offer suppliers the opportunity to expand their production.

CHALLENGES ARISING FROM THE COMPETITION WITH NON-FOSSIL AND (OTHER) FOSSIL FUELS

Role as a Bridge Fuel

As a fossil fuel cleaner than coal but dirtier than renewables, natural gas could suffer the fate of Buridan’s donkey if its diffusion in India is not managed well. Energy analysts — at least those who position natural gas as a “bridge fuel” — argue that ample supplies of natural gas in global markets will sustain the prevailing trend of low prices, at least in the near future. This is indeed true. Consider this: reflecting the decadal growth in global crude oil discoveries, global proven reserves of natural gas rose from 187.1 trillion cubic metres (TCM) in 2011 to 198.8 TCM in 2019.[46] The market, which is awash with shale gas from the USA and natural gas from newly-developed fields in Russia, Australia, and China, is currently witnessing reduced demand following the outbreak of the COVID-19 pandemic. Hence, apart from ballooning demand after the world emerges completely out of the shadow of lockdowns, any other future price spikes, apart from the annual weather-driven demand escalations, would probably originate from demand in countries of the Indo-Pacific, which are considering an expansion of natural gas imports.

Threat of “Technological Lock-in”

Climate-change experts contend that price complexities and a need for massive financial and technical support make natural gas more of a short-term substitute fuel. Its transitionary disposition to act as a “bridging fuel” to simultaneously meet the energy security needs of a country along with local pollution mitigation could increase the threat of a “technological lock-in”.[47] This is a scenario wherein any development in new energy systems stagnates on account of past investments in entrenched technologies.[48] Chandra Bhushan, Chief Executive Officer (CEO) of the International Forum for Environment, Sustainability & Technology (Iforest) uses this template to suggest that the prevalence of institutional support and the length of the value chain to supply one unit of energy are the principal factors that determine how sustainable a fuel really is. To accentuate his point, he questions the viability of expanding the national natural gas grid — under the “One Nation One Gas Grid” — even as India has amplified its renewable energy target to 450 GW by 2030. He summarises his argument by saying, “The idea of the energy transition will have to be juxtaposed with political considerations, which will prove more of a challenge to surpass than the transition to low-carbon fuel sources.”

On the other hand, Jitendra Roychoudhury, Research Fellow, King Abdullah Petroleum Studies and Research Center (KAPSARC), counters this narrative by arguing:

“The competition between fuels is not an apple-to-apple comparison. Even though climate change analysts may feel that the transition to a gas-based economy may be a wasted development, bidding for expanding the CGD network is still going strong. As far as pricing is concerned, even prices set by the Government of India (with regard to domestic natural gas) are periodically revised. These developments underscore the significance of the market and its realisation of the tough road ahead for the transition to renewables.”[49]

Until 2019, the PNGRB extended CGD “coverage” to 228 Geographical Areas (GAs), covering 402 out of India’s 718 districts, through the 10th CGD Bidding Round. Approximately 70 per cent of India’s population resides in these GAs. Apart from laying more than 58,000 kilometres of steel pipeline, this “coverage” includes the addition of approximately 20 million domestic PNG connections and more than 3,500 CNG fuelling stations by 2029.[50] The forthcoming 11th Round will be developed around a pipeline from Mumbai, on the west coast, to Angul (Odisha), on the east coast. Furthermore, the Union Minister for Petroleum & Natural Gas and Steel, Mr Dharmendra Pradhan, expects to develop 10,000 CNG fuelling stations by 2025.[51]

Obscuring the Clean Energy Transition in the Transportation Sector

CNG-fuelled vehicles emit smaller amounts of greenhouse gases (GHG) such as carbon monoxide, carbon dioxide, nitrogen oxides, and particulate matter, than do vehicles that run on liquid fuels. Yet, even as natural gas’s role in air-pollution mitigation is extolled by local governments, the adoption of CNG-fuelled vehicles has not fared well.[52] The sale of these vehicles is restricted by the geographical distribution of CNG fuelling stations in states that are connected to the national natural gas grid. Moreover, these vehicles require larger fuel tanks (that are stored in the boot space) than their liquid fuel-running competitors because the latter deliver three-quarters more energy per litre.[53] Consequently, despite empathising with air-pollution mitigation and climate-change objectives — the well-known “co-benefits” of natural gas adoption — consumers often opt for vehicles running on petrol or diesel.[54] Such limitations have presently constrained its mass adoption largely to urban public transport services. Given these arguments, the successful adoption of CNG will depend on the pace of expansion of distribution infrastructure and the implementation of other associated policies, such as tax rebates, that will bring down the cost of CNG-fuelled vehicles (factory-fitted CNG-fuelled vehicles are more expensive than petrol and diesel variants).

However, what are the implications of India’s much-debated plan to scale up the penetration of Electric Vehicles (EVs) to 30 per cent by 2030?[55] CNG, which is less expensive than diesel and petrol, could derail the National E-Mobility Programme’s objective of saving more than 300,000 barrels of oil per year and reducing carbon emissions by 0.5 tonnes annually. With only 933 EV charging stations (0.1 per cent of the world total), the need for a competitive EV policy that blends the advantage of CNG dispersion with the overall effort to reduce crude oil consumption is the need of the hour.[56]

Weak Resistance to Coal

What about coal? The fuel which natural gas substituted to meet the heating and lighting needs of most developed economies has proven much more resilient in a developing economy like India. Unsurprisingly, the second component of India’s energy strategy, mentioned earlier in this article, stresses the efficient consumption of coal. So, why is this not surprising? A close examination of India’s Intended Nationally Determined Contribution (INDC), which was submitted to the United Nations Framework Convention on Climate Change (UNFCCC) as part of the Paris Agreement of 2015, has no mention of natural gas.[57] It, however, commits to the implementation of Clean Coal policies — including supercritical technologies for coal-based power plants — among several other mitigation measures. Indeed, in the intervening period, India has mirrored the trend among other Asian economies by encouraging intensive coal use through the increase in the share of coal within the total installed capacity of power stations, from 185.17 GW in FY 2015–16 to 202.67 GW in FY 2020–21.[58] This is particularly worrying, given that renewables (wind + solar), which have received tremendous institutional and financial support since 2015, have only minimally impacted the dominance of coal in the country’s primary energy mix (see Figure 2).

RECENT ALTERATIONS TO INDIA’S STRATEGY FOR ESTABLISHING A GAS-BASED ECONOMY

The Promise of the Future?

The success of any energy source in India requires close policy support and reforms (commitment). For instance, the absence of a coherent policy on EVs has frustrated the industry’s attempt to expand manufacturing capacities. Likewise, the recent interest in its development notwithstanding, natural gas must overcome severe apprehensions by end-use customers in India. India’s power generation industry has already burned its fingers once. Despite increasing LNG imports, continued idle gas-fired capacity indicates that pricing will play a significant role in changing this commodity’s image of a disruptive fuel undergoing an identity crisis. It could either outdo clean and emerging sources of energy or succumb to more secure and established indigenous fuels like coal. Thus, the pathway to a gas-based economy is contingent on the realisation of the following:

Infrastructure. In February 2021, Prime Minister Narendra Modi announced the infusion of Rs 7.5 trillion (US$ 100 billion) over five years to expand oil and gas infrastructure in India with a stated aim to encourage the adoption of clean — albeit conventional — fuels and reduce the reliance on imports.[59] Of this amount, about US$ 9.5 billion is already earmarked under the “One Nation One Gas Grid” scheme for the development of infrastructure dedicated to natural gas production, transport and re-gasification on the east coast. In particular, the Gas Authority of India Limited (GAIL) hopes to develop 17,000 kilometres of pipeline networks in this region.

India should also prioritise capability enhancement in the field of LNG carrier construction. It could invite domestic stakeholders to enter into a Public-Private Partnership (PPP) to share the costs of projects and thereby manage risk under the Atmanirbhar Bharat scheme. As global demand for this fuel increases, the corresponding stress on transport will be visible along with the need to access supplies from geopolitically sensitive regions.

Interest by Private Players. Following India’s declared intent to transition to a gas-based economy, the joint-venture between RIL and British Petroleum (BP) commenced the production of gas from the R Cluster — the first of three deep-water projects in the Reliance-owned KG-D6 field. According to media reports, the output from this field alone is expected to form 10 per cent of the country’s current production from domestic fields.[60] An outcome of the Open Acreage Licensing Policy (OALP) under the Hydrocarbon Exploration and Licensing Policy (HELP) which succeeded the NELP, contractors may exploit blocks that are not included in the tender. Private players will keenly observe the operations of the RIL–BP joint venture to measure the government’s commitment to allow a level playing field.

Pricing and Tariff Structure. The promulgation of the Natural Gas Marketing Reforms in October 2020 will enable what is termed the “market price discovery of natural gas”.[61] Under this provision, contractors are allowed to sell natural gas through a supervised online bidding process that will ensure transparency. Further, to avoid price manipulations, subsidiaries or affiliates of the seller will not be able to participate in the bidding process.

The most important aspect of these reforms is that contractors will now not be compelled to sell their product to public sector entities. Instead, they may sell their product to any buyer in the world as long as both parties participate in the supervised online bidding process. A complement to the pricing freedom allowed under the Production Sharing Contract (PSC), these measures will allow contractors to recover their investments at a quicker pace.

The PNGRB has also introduced a unified gas tariff structure to transport natural gas via the National Gas Grid. On the one hand, seeking to incentivise the adoption of natural gas in India’s interior regions with investments for the expansion of the gas grid, this policy levies a higher tariff on a consumer within 300 kilometres of an LNG terminal or gas field.[62] On the other hand, the introduction of such a tariff system would lead to cross-subsidisation and reduced savings for industrial units along the west coast.

CONCLUSION

Although the target to expand the share of natural gas in India’s primary energy mix to 15 per cent by 2030 and the objective of creating a “gas-based economy” are the leitmotifs of this study, the conceptual disconnect between them is undeniable. A gas-based economy implies the dominance of natural gas in India’s primary energy mix. This objective depends on the success of India’s efforts to augment natural gas supply from indigenous sources. In this scenario, the target to increase the share of natural gas in the primary energy mix appears incapable of supporting the shift.

Capacity enhancements are already underway. The expansion of the transmission network before the discovery of new indigenous supplies resembles the overconfidence of the last decade when surplus, and eventually, underutilised gas-fired power-plant capacity was developed. In contrast, additional LNG terminal capacity will be significant if India fails to locate ample indigenous supplies of natural gas. Furthermore, the success of India’s LNG diversification strategy depends on the pattern of low spot prices due to the prevailing supply glut. The diffusion of natural gas through CGD will shrink high oil imports marginally, but at the same time, it will also increase its susceptibility to price shocks that arise from increasing global demand and geopolitical disturbances. Hence, with India’s decarbonisation efforts hanging in the balance, and the looming reality of additional import dependence, India’s policymakers will have to outline a detailed roadmap for the absorption of greater LNG imports or indigenous supplies into the economy.

****************

About the Author:

Dr Oliver Nelson Gonsalves is an Associate Fellow and the Head of the Maritime Energy-Security and Security-of-Energy (MESSE) Cluster at the National Maritime Foundation (NMF). He leads the NMF’s study into the maritime facets of energy. He can be contacted at associatefellow1.nmf@gmail.com

Endnotes:

[1] According to Speight, “the term natural gas is the generic term that is applied to the mixture of gaseous hydrocarbon derivatives and low-boiling liquid hydrocarbon derivatives that is commonly associated with petroliferous (petroleum-producing, petroleum-containing) geologic formations”. James G Speight, Natural Gas: A Basic Handbook (Cambridge, MA: Elsevier, 2019), 4. Methane is the main constituent of natural gas along with propane, butane, and pentane, which may be found in natural-gas liquids.

[2] Asia Pacific Energy Research Centre, A Quest for Energy Security in the 21st Century (Tokyo: Institute of Energy Economics, 2007), 1–100. https://aperc.or.jp/file/2010/9/26/APERC_2007_A_Quest_for_Energy_Security.pdf

[3] Due to its natural occurrence — in varying proportions — in natural gas fields, oil fields, tight rock formations (like shale rock), and biological sources (landfills and bio-gas plants), natural gas is separated into two categories. Conventional gas is found in geological formations that are highly permeable (porous) and can be extracted through traditional methods (vertical and slant drilling). Unconventional gas is found in formations with less permeability and can be recovered only through non-traditional methods, such as hydraulic fracking, horizontal drilling, and so forth. Gas hydrates, shale gas, coalbed methane, bio-gas are examples of un-conventional gas.

[4] Speight, Natural Gas, 361.

[5] Shawn Olson Hazboun and Hilary Schaffer Boudet, “Natural Gas – Friend or Foe of the Environment? Evaluating the Framing Contest over Natural Gas through a Public Opinion Survey in the Pacific Northwest”, Environmental Sociology (March 2021): 9–10, https://doi.org/10.1080/23251042.2021.1904535

[6] British Petroleum, Statistical Review of World Energy 2011, 60th Edition, 20, and Statistical Review of World Energy 2020, 69th Edition, 4. http://large.stanford.edu/courses/2011/ph240/goldenstein1/docs/bp2011.pdf

[7] The State Council, “Notice of the State Council on Issuing the Air Pollution Prevention and Control Action Plan”, People Republic of China, No 37 (September 2013), http://www.gov.cn/zwgk/2013-09/12/content_2486773.htm

[8] Group of Ministers, India Hydrocarbon Vision-2025 (Government of India, 2000), 4–5. http://petroleum.nic.in/sites/default/files/vision.pdf. See also, Kapil Narula, The Maritime Dimension of Sustainable Energy Security (Singapore: Springer Nature, 2019), 106–108. Natural gas, in its gaseous form, is refrigerated at –162 °C to create a liquid consistency at a liquefaction plant near the source of supply before being transferred to an LNG carrier. In its liquid form, that is, LNG, natural gas is reduced by 600 times, which makes it easy to transport over long distances in insulated tanks on board LNG carriers. Once the ship reaches the re-gasification terminal at the destination port, the LNG is re-gasified for transport using pipelines.

[9] Planning Commission, Integrated Energy Policy: Report of the Expert Committee (Government of India, Delhi, August 2006): 44.

[10] Ministry of Petroleum & Natural Gas, “Shri Dharmendra Pradhan Chairs First Meeting of Consultative Committee of Ministry of Petroleum & Natural Gas”, Press Information Bureau, Government of India, Delhi, 06 December 2019.

[11] Narendra Modi, “Text of PM’s Address at the Inauguration of India Energy Forum”, Prime Minister’s Office, Press Information Bureau, Government of India, Delhi, 26 October 2020.

[12] Narendra Modi, “India Energy Forum”.

[13] P R Shukla et al., “Assessment of Demand for Natural Gas from the Electricity Sector in India”, Program on Energy and Sustainable Development, Working Paper, No 66 (October 2007): 1. https://www.researchgate.net/publication/316928381_Natural_Gas_in_India_An_Assessment_of_Demand_from_the_Electricity_Sector

[14] Natural-gas-based power plants have faster ramp-up rates that lend flexibility to the electricity grid in the case of a sudden spike in demand. It is also used as a feedstock (raw material) to manufacture ammonia-based urea, a widely used fertiliser in India.

[15] Rahul Tongia, “Revisiting Natural Gas Imports for India”, Economic and Political Weekly 40, No 20 (14–20 May 2005): 2032–2033. Compressed Natural Gas (CNG), a derivative of natural gas, comprises methane stored at high pressure and ambient temperature. Natural gas may be converted to CNG by compressing it to 3000 psi (pound-force per square inch) to 1 per cent of the volume the gas would occupy at normal atmospheric pressure. In this form, it can feed an internal combustion engine and act as an alternative to petrol and diesel. Liquefied Petroleum Gas (LPG) is a natural gas liquid (NGL) comprising propane and butane, whereas natural gas from KG-D6 comprises primarily methane, which feeds fertiliser production.

[16] Reliance Industries Limited, “India Has Never Been Here Before: Facts You Didn’t Know about KG-D6,” Flame of Truth Series (2014): 7. In the case of deep-water exploration projects, the average project timeline from discovery to production is 10 years.

[17] National Statistical Office, Government of India, Ministry of Statistics and Programme Implementation, Energy Statistics 2021, No. 28, 89. file:///E:/Jobs/Master%20Data_Oliver/India_Energy%20Statistics_MoSPI_2011-20/Energy%20Statistics%20India%202021.pdf

[18] Sanjay Kumar Kar and Ayush Gupta, eds., Natural Gas Markets in India: Opportunities and Challenges (Singapore: Springer Nature, 2019), vii.

Data from 2017–18 in Energy Statistics 2019 (page 97) indicates that the total share of Renewable Energy and Others (including nuclear energy) was –0.67 per cent. This document calculates the share of fuels in energy by weighing the relation between consumption/production of the fuel with total energy use or production. Based on this explanation, the author assumes that biomass (cow dung and wood), which comprises a large share of renewable energy in India, was greatly displaced by the introduction of Liquefied Petroleum Gas (LPG) subsidies, starting in 2016, to 50 million households under the Pradhan Mantri Ujjwala Yojana (PMUY) scheme. Intensified LPG-use is reflected in the surge in the share of crude oil.

[19] Manish Vaid and Sanjay Kumar Kar, “India’s Active Engagement with Natural Gas: Imperatives and Challenges”, in Natural Gas Markets in India: Opportunities and Challenges, eds Sanjay Kumar Kar and Ayush Gupta (Singapore: Springer Nature, 2019), 13.

[20] Twesh Mishra, “India Saved over Rs 30,000 Cr despite Rising Petro Product Imports in FY21”, Business Standard, 22 April 2021. https://www.business-standard.com/article/economy-policy/india-saved-over-rs-30-000-cr-despite-rising-petro-product-imports-in-fy21-121042201160_1.html

[21] Data for Crude and Products, Petroleum Planning & Analysis Cell, Ministry of Petroleum & Natural Gas, Government of India. https://www.ppac.gov.in/content/212_1_ImportExport.aspx

See also: “Share of Leading Commodities Imported by India in Financial Year 2020”, Statista, accessed June 05, 2021, https://www.statista.com/statistics/650509/share-of-imports-by-commodities-india/

[22] Petroleum Planning and Analysis Cell, “Gas Price Ceiling for the Period April, 2021-September, 2021”, Ministry of Petroleum and Natural Gas, Government of India, 31 March 2021. https://www.ppac.gov.in/WriteReadData/userfiles/file/Gas%20Price%20Ceiling%20for%20the%20period%20April%202021%20to%20September%202021.pdf

See also: Press Trust of India, “India Wants Qatar to Lower Gas Price; Qatar Says No to Reopening Existing Contracts”, The Economic Times, 28 January 2020. https://energy.economictimes.indiatimes.com/news/oil-and-gas/india-wants-qatar-to-lower-gas-price-qatar-says-no-to-reopening-existing-contracts/73683411

[23] Sambit Mohanty and Srijan Kanoi, “LNG’s Unprecedented Surge to Apply Brakes on India’s Imports, Consumption”, S&P Global Platts, accessed April 24, 2021, https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/011121-lngs-unprecedented-surge-to-apply-brakes-on-indias-imports-consumption

[24] Petroleum Planning and Analysis Cell, “Import of Liquefied Natural Gas”, Financial Year 2020–21 (April to March), Ministry of Petroleum and Natural Gas, Government of India.

[25] Sanjay Kumar Pradhan (2020), India’s Quest for Energy through Oil and Natural Gas Trade and Investment, Geopolitics, and Security (Singapore: Springer Nature), 151–170.

[26] David G Victor, “Natural Gas and Geopolitics,” in Security of Energy Supply in Europe: Natural Gas, Nuclear and Hydrogen, eds Francois Leveque, Jean-Michel Glachant, Julián Barquín, Christian von Hirschhausen, Franziska Holz and William J Nuttall (Cheltenham: Edward Elgar Publishing Limited, 2010), 91–92.

[27] The Shipping Corporation of India, “Tankers”, accessed June 02, 2021, https://www.shipindia.com/services/servicepage/specialized-vessels

[28] In 2020, the cost of a 215,000 m³ LNG carrier was US$ 250 million. Read: M Habib Chusnul Fikri et al., “Estimating Capital Cost of Small Scale LNG Carrier”, Proceedings of the 3rd International Conference on Marine Technology, (2020): 225–226. doi: 10.5220/0008542102250229

[29] Ross Wyeno and Josh Zwass, “Spotlight: LNG Charter Rates Drop to Record Lows, Support Strong US LNG Dispatches This Spring”, S&P Global Platts, accessed May 17, 2021, https://www.spglobal.com/platts/en/market-insights/latest-news/shipping/031021-spotlight-lng-charter-rates-drop-to-record-lows-support-strong-us-lng-dispatches-this-spring

[30] National Statistical Office, Ministry of Statistics and Programme Implementation, Government of India, Energy Statistics 2020, No. 27, 65. “Current List of Gas Power Plants”, Global Energy Observatory, accessed October 13, 2020, http://globalenergyobservatory.org/list.php?db=PowerPlants&type=Gas

[31] Apart from its uses in electricity generation, transport, cooking, and heating, natural gas is also used as a raw material for the production of fertiliser, dyes, paints, medicines, photographic films, explosives, plastics and anti-freeze.

[32] Press Information Bureau, Ministry of Petroleum & Natural Gas, Government of India, “Demand and Supply of Natural Gas”, January 07, 2019, https://pib.gov.in/Pressreleaseshare.aspx?PRID=1558885

[33] S Can Gülen, Gas Turbines for Electric Power Generation (Cambridge: Cambridge University Press, 2019), 2.

[34] Central Electricity Regulatory Commission, Notification Number No. L-1/144/2013/CERC, dated February 21, 2014, 14.

[35] Gülen, Gas Turbines for Electric Power Generation, 2. In a combined-cycle power plant, which is primarily fed by natural gas, the waste heat generated by the gas turbines after the production of electricity is re-routed to steam turbines to produce additional electricity. In this way, a combined-cycle power plant can produce approximately 50 per cent more electricity than its predecessor, the simple-cycle gas plant.

[36] Standing Committee on Energy, Stressed/Non-Performing Assets in Gas based Power Plants, 42nd Report, Ministry of Power (New Delhi: Lok Sabha Secretariat, 2018), 8.

[37] Standing Committee on Energy, Stressed/Non-Performing Assets in Gas based Power Plants, 11–13.

[38] Lydia Powell and Akhilesh Sati, “Natural Gas in India: From Cinderella to Goldilocks”, accessed March 21, 2021, https://www.orfonline.org/expert-speak/natural-gas-india-cinderella-goldilocks-66385/

[39] Department of Commerce, Ministry of Commerce & Industry, Government of India, “Export-Import Data Bank”, 2000. https://tradestat.commerce.gov.in/eidb/default.asp This purchase could have originated from a third party and resold to India at the Zeebrugge Hub in Belgium.

[40] Department of Commerce, “Export-Import Data Bank”, 2004. https://tradestat.commerce.gov.in/eidb/default.asp

[41] Department of Commerce, Ministry of Commerce & Industry, Government of India, “Export-Import Data Bank”, 2021. https://tradestat.commerce.gov.in/eidb/default.asp

[42] Department of Commerce, “Export-Import Data Bank”, 2021.

[43] International Energy Agency, India 2020: Energy Policy Review, (2020): 271–282.

[44] Hazboun and Boudet, “Natural Gas”, 10.

[45] Saurabh Kumar, “Why Indian Investments in Mozambique Are Facing Bad Weather”, The Financial Express, 20 January 2018. https://www.financialexpress.com/economy/why-indian-investments-in-mozambique-are-facing-bad-weather/1022670/

[46] British Petroleum, Statistical Review of World Energy 2011, 32.

[47] Chandra Bhushan, “SDGs for Energy Security and Governance – Examining Impact of Energy on SDG Goals in India”, online panel-discussion on Climate Change and Sustainable Development in India’s Energy Security Agenda, webinar organised by The Energy and Resources Institute (TERI), 19 November 2020.

[48] Timothy J Foxon, “Technological and Institutional ‘lock-in’ as a barrier to sustainable innovation”, ICCEPT Working Paper (November 2002): 2–4, https://www.imperial.ac.uk/media/imperial-college/research-centres-and-groups/icept/7294726.PDF

[49] Jitendra Roychoudhury, “SDGs for energy security and governance – Examining impact of energy on SDG goals in India,” online panel-discussion on Climate change and sustainable development in India’s energy security agenda, webinar organised by The Energy and Resources Institute (TERI), 19 November 2020.

[50] Press Release by the Petroleum and Natural Gas Regulatory Board, New Delhi, accessed February 22, 2019, https://www.pngrb.gov.in/pdf/cgd/bid10/PressRelease26022019.pdf

[51] Press Trust of India, “India to Launch 11th City Gas Licensing Round Soon: Dharmendra Pradhan”, Livemint, 10 September 2020. https://www.livemint.com/industry/energy/india-to-launch-11th-city-gas-licensing-round-soon-dharmendra-pradhan-11599730402140.html

[52] “What is the Status of Air Pollution in Delhi?”, Q&A, Centre for Science and Environment, accessed May 21, 2021, https://www.cseindia.org/what-is-the-status-of-air-pollution-in-delhi-835

[53] Speight, Natural Gas, 20–21.

[54] According to Mayrhofer and Gupta (2016), co-benefits may refer to “the positive effects that a policy or measure aimed at one objective might have on other objectives, irrespective of the net effect on overall social welfare”. Jan P Mayrhofer and Joyeeta Gupta, “The Science and Politics of Co-benefits in Climate Policy”, Environmental Science and Policy 57 (2016): 22–30, http://dx.doi.org/10.1016/j.envsci.2015.11.005

[55] Ronak Shah, “Government Finally Wakes up: Sets a Realistic Goal of 30% Electric Vehicles by 2030 from Existing 100% Target”, The Financial Express, 08 March 2018. https://www.financialexpress.com/auto/car-news/government-finally-wakes-up-sets-a-realistic-goal-of-30-electric-vehicles-by-2030-from-existing-100-target/1091075/

[56] Shalini Sharma, “India Has So Far Installed 933 EV Charging Stations across the Country: CEA”, PSU Watch, accessed May 01, 2021, https://psuwatch.com/india-installed-ev-charging-stations-933-cea#

[57] “India’s Intended Nationally Determined Contribution: Working Towards Climate Justice”, INDCs as communicated by Parties, United Nations Framework Convention on Climate Change, accessed May 04, 2021, https://www4.unfccc.int/sites/ndcstaging/PublishedDocuments/India%20First/INDIA%20INDC%20TO%20UNFCCC.pdf

[58] Central Electricity Authority, “Installed Capacity Report, March 2016 and March 2021”, Ministry of Power, Government of India, accessed April 29, 2021, https://cea.nic.in/installed-capacity-report/?lang=en

[59] T E Narasimhan, “India to Spend Rs 7.5 Trillion on Oil and Gas Infra in Next 5 Yrs: PM Modi”, Business Standard, 17 February 2021. https://www.business-standard.com/article/economy-policy/india-to-spend-rs-7-5-trillion-on-oil-and-gas-infra-in-next-5-yrs-pm-modi-121021700989_1.html

[60] Karunjit Singh, “Explained: What Start of Gas Production in KGD6 Means for India”, The Indian Express, 20 December 2020. https://indianexpress.com/article/explained/explained-what-start-of-gas-production-in-kgd6-means-for-india-7110542/

[61] Ministry of Petroleum and Natural Gas, “Natural Gas Marketing Reforms,” The Gazette of India, October 15, 2020. http://dghindia.gov.in/assets/downloads/5ffbe7fa78f17NaturalGasMarketingReforms15102020.pdf

[62] Press Trust of India, “Oil Regulator PNGRB Simplifies Gas Pipeline Tariff”, The Indian Express, 26 November 2020. https://economictimes.indiatimes.com/industry/energy/oil-gas/oil-regulator-pngrb-simplifies-gas-pipeline-tariff/articleshow/79431453.cms?from=mdr

The Indian navy Shivalik-class stealth multi-role frigate INS Kamorta (F49) and the Japan Maritime Self-Defense Force Akizuki-class destroyer JS Fuyuzuki (DD 118) underway in formation during exercise Malabar 2018. Malabar is designed to advance military-to-military coordination in a multinational environment between the U.S., Japanese, Indian and now Australian maritime forces. (U.S. Navy photo by Mass Communication Specialist 2nd Class Sarah Myers/Released)

The Indian navy Shivalik-class stealth multi-role frigate INS Kamorta (F49) and the Japan Maritime Self-Defense Force Akizuki-class destroyer JS Fuyuzuki (DD 118) underway in formation during exercise Malabar 2018. Malabar is designed to advance military-to-military coordination in a multinational environment between the U.S., Japanese, Indian and now Australian maritime forces. (U.S. Navy photo by Mass Communication Specialist 2nd Class Sarah Myers/Released)

THE NEW YORK TIMES

THE NEW YORK TIMES ")

Leave a Reply

Want to join the discussion?Feel free to contribute!