GEOPOLITICS OF WEST ASIA & CLIMATE CHANGE AS COMPELLING DRIVERS OF INDIA’S SHIFT TO RENEWABLE RESOURCES OF ENERGY

This article is an integral part of the series of major research-studies on the maritime facets of India’s energy security, being undertaken at the National Maritime Foundation. This portion of the research-study, which advocates the adoption of hydrogen-fuel by India as its option-of-first-choice (the current obsession with solar power notwithstanding) is being presented in three parts. This article constitutes Part 1, which seeks to set the stage, so-to-speak, by presenting the troubled and troublesome geopolitics of West Asia, exacerbated by the impact of climate-change, as a compelling driver for India’s shift towards clean and renewable sources of energy.

India’s Primary Energy Basket & Fossil Fuel Imports from West Asia

Large countries, particularly those with rapidly growing economies, find it difficult to delink energy from their economic growth.[1] The rapid pace of economic growth in large, middle-income, emerging economies in particular, implies a larger demand for energy resources and related consumption.[2] Hence, energy security for an emerging economy is of strategic importance.[3] This is true for a number of large, rapidly-growing contemporary economies such as those of China and India.[4] Figure 1 depicts India’s basket of sources of primary energy in 2019-20,[5] and shows that the largest share in India’s primary-energy basket is coal, followed by crude-oil.

|

Coal

Although India is the second-largest producer of coal, it is also the second-largest importer of coal on the planet.[6] There are two basic reasons for this import: The first is that as the Indian economy grows, coal demand is continuously outstripping indigeneous supply. According to the Annual Report (2019-20), “Demand for coal for 2019-20 was estimated at 1000 million tonnes against which, actual supply of coal in 2019-20 up to December, 2019 (provisional) was 695.49 Mte”.[7] The second is the poor quality of Indian coal — both, ‘coking coal’ (used for metallurgical purposes), and, ‘non-coking coal’ (such as ‘thermal coal’ a.k.a. ‘steaming coal’, which is so named because it is used to generate steam, mainly for the production of electricity and, to a somewhat lesser extent, cement). The quality of coking coal is dependent upon the ash content of the coal. The higher the ash content, the poorer is the quality. Indian coal has generally high ash content that exceeds 40%.[8] The gradation of non-coking coal is based on Gross Calorific Value (GCV). High amounts of moisture and ash-content lower the GCV. The lower the GCV, the poorer the coal.

15 countries account for 99.6% of the imports of coal by India: Australia, Indonesia, South Africa, the USA, Canada, Russia, Mozambique, Singapore, the UAE, Switzerland, New Zealand, China, Latvia, the Netherlands, and the UK.[9] It is important to note that barring China, none of these import-sources are located in areas of acute geopolitical turbulence, particularly such turbulence as might deteriorate into armed conflict. This is a why India’s vulnerability and geopolitical sensitivity in the case of coal imports are so very much lesser than those attending the import of crude-oil, where the geopolitical situation is more fragile by several orders of magnitude.

Crude Oil

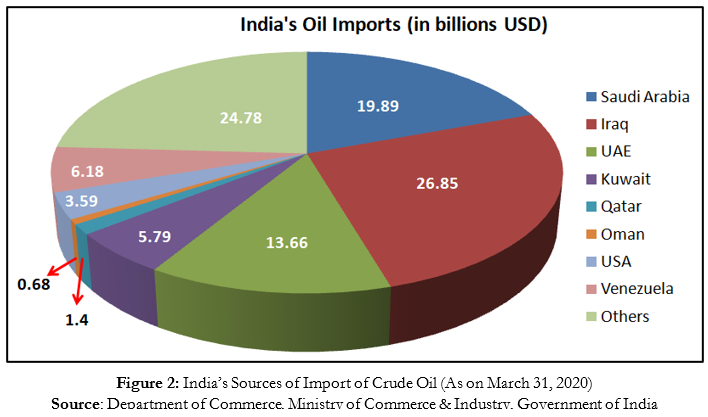

Insofar as crude-oil is concerned, India’s import dependence is even higher than that in the case of coal. India is the third largest importer of crude oil in the world, next only to China and the United States,[10] and has an especially heavy dependence on imports from West Asia (a.k.a. the ‘Middle East’).[11] As depicted in Figure 2, two-thirds of India’s crude oil imports are sourced from countries in West Asia with Iraq contributing the highest, followed by Saudi Arabia, United Arab Emirates, Qatar etc.[12]

|

Natural Gas

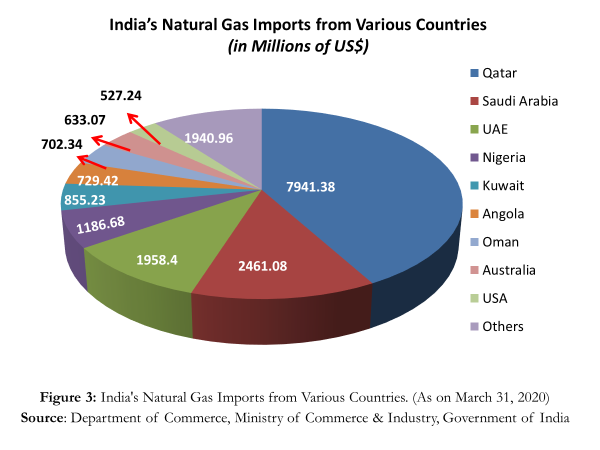

Natural gas is another fossil-fuel resource that is extremely important for India’s energy security. Natural gas is used both as feedstock[13] (i.e., for the production of ammonia, which is then converted into urea) and as a source of energy for the generation of electricity. It is especially vital for India’s fertilizer sector, within which it is used as feedstock. As of 2016, 43% of natural gas in India was used as feedstock, while 32% was used for the production of electricity.[14] Both these values are predicted to rise in the years ahead. The population of India, which is already in excess of 1.3 billion people, is predicted to overtake that of China during the course of the coming decade.[15] These people will need to be fed. The consequent requirement to produce more food per acre of land that is cultivated will drive an increase in the demand for ammonia-based fertilizer (urea). As the population rises, there will also be an increase in the base demand for electricity. All sources of electric power generation will witness a rise in demand and this will hold true for natural gas as well. Since close to 75% of India’s natural gas imports are sourced from West Asia, the geopolitical moves and countermoves being played out in this sub-region have, once again, obvious and significant strategic implications for New Delhi. Figure 3 depicts the top ten sources of India’s import of natural gas.[16]

This demand for crude oil and natural gas gets compounded by several factors, including the volatility of oil markets and the associated price-fluctuation. In the aftermath of the Covid-19 pandemic, for instance, global and regional demand for oil and natural gas dropped substantially. Russia and the OPEC countries wanted to adopt a united stand, but the USA was clearly playing to its own interests and even threatened its ally Saudi Arabia that it could face tariff actions if it did not cut oil-production in order to help the USA’s own shale-oil industry, which needed higher prices to break even. The US-Russian animosity introduced its own set of unhelpful dynamics into this already simmering geopolitical cauldron.[17] All this impacts India very substantially, especially given the high potential for armed conflict in West Asia.[18] Indeed, the ongoing conflict in Yemen and its impact upon the Strait of Bab-el-Mandeb offers a precursor that is, in and of itself, frighteningly ominous. Any deterioration in the situation that allows the present vituperative polemics to drift into military action can lead to serious disruptions of oil-bearing shipping flowing along some of the most important of the international shipping lanes (ISL)of the world. This would compel New Delhi to define new Sea Lines of Communication (SLOCs)[19] as it scrambles for energy resources elsewhere.[20]

If all these were not problems enough, the global dependence of fossil fuels for energy production has also resulted in an anthropogenic impact on climate leading to climate change.[21] Climate change and its maritime impacts such as sea level rise,[22] ocean acidification,[23] etc., can only be mitigated by reducing the overall carbon footprint. This reduction in the carbon footprint requires reducing the dependence on fossil fuels and adopting alternative sources of ‘clean’ energy.[24] According to the 2015 Paris climate change agreement, India is obligated to meet 40% of its energy demand using clean energy sources by the year 2030, in order to achieve the current climate targets.[25] Sustainable Development Goal #7 (SDG #7) enjoins countries to focus upon using “Affordable and Clean Energy” to drive their economies.[26]

How this might best be done and where exactly hydrogen-fuel fits in, are the very subjects of the next article in this ongoing series.

*Sameer Guduru is an Associate Fellow at the National Maritime Foundation. He can be contacted at associatefellow3.nmf@gmail.com

Endnotes

[1] T Wang, “Top 20 countries in primary energy consumption in 2018”, https://www.statista.com/statistics/263455/primary-energy-consumption-of-selected-countries/

[2] Omer Esen and Metin Bayrak, “Does More Energy Consumption Support Economic Growth in Net Energy-importing Countries?”, Journal of Economics, Finance and Administrative Science 22 (2017), 75-98.

[3] Gunnar Fermann, “What is Strategic about Energy? De-simplifying Energy Security” in Moe E., Midford P. (eds) ‘The Political Economy of Renewable Energy and Energy Security. Energy, Climate and the Environment’, (Palgrave Macmillan, London, 2014), 21-45.

[4] Samir Tata, “Deconstructing China’s Energy Security Strategy”, https://thediplomat.com/2017/01/deconstructing-chinas-energy-security-strategy/

Ashok Sharma, “India’s Quest for Energy Security”, https://www.dailypioneer.com/2020/sunday-edition/india—s-quest-for-energy-security.html

[5] Government of India, Ministry of Commerce & Industry, Department of Commerce, https://commerce-app.gov.in/eidb/

[6] Mining Technology, “Countries with the Biggest Coal Reserves”, https://www.mining-technology.com/features/feature-the-worlds-biggest-coal-reserves-by-country/

[7] Government of India, Ministry of Coal, “Annual Report 2019-2020”, Chapter 6 Coal and Lignite Production. https://coal.nic.in/sites/upload_files/coal/files/coalupload/AnnualReport2019-20/Chapter6-en.pdf

[8] Swagat Bam, Lydia Powell and Akhilesh Sati, “Coal Beneficiation: Status and Way Forward”, ORF Policy Brief, 05 July 2017, https://www.orfonline.org/research/coal-beneficiation-in-india-status-and-way-forward/

[9] Daniel Workman, “Coal Imports by Country: India”, World’s Top Exports Website, http://www.worldstopexports.com/crude-oil-imports-by-country/ (accessed 05 May 2020)

[10] Workman, “Crude Oil Imports by Country: India”, World’s Top Exports Website, http://www.worldstopexports.com/crude-oil-imports-by-country/ (accessed March 9,2020)

[11] PTI New Delhi. “Crude oil imports from the US jump 72%, Iraq is top supplier” https://www.thehindubusinessline.com/markets/commodities/oil-imports-from-us-jump-72-per-cent-iraq-is-top-supplier/article29531296.ece# (accessed September 27, 2019)

[12] Government of India, Ministry of Commerce & Industry, Department of Commerce, https://commerce-app.gov.in/eidb/

[13] The term ‘feedstock’ denotes any renewable, biological material that can either be used directly as a fuel, or, can be converted to another form of fuel or energy product.

[14]Gulf Petrochemicals and Chemicals Association, “Changes in India’s Natural Gas Market and Implications for the Fertilizer Industry”, 2017, https://gpca.org.ae/wp-content/uploads/2018/03/Changes-in-Indias-Natural-Gas-Market-and-Implications-for-the-Fertilizer-Industry.pdf

[15] Panjab Singh, “Feeding 1.7 billion”, Presidential Address, Founding Day and 26th General Body Meeting, National Academy of Agricultural Sciences, New Delhi, June 5, 2019

[16] Government of India, Ministry of Commerce & Industry, Department of Commerce, “Export-Import Data Bank”. https://commerce-app.gov.in/eidb/

[17] Kalyeena Makortoff, “Oil Prices Fall Again despite OPEC+ Deal to Cut Production”, https://www.google.com/amp/s/amp.theguardian.com/business/2020/apr/10/opec-russia-reduce-oil-production-prop-up-prices

[18] Anisur Rahman, “Geopolitics of West Asia: Implications for India”, https://www.financialexpress.com/defence/geopolitics-of-west-asia-implications-for-india/1664354/

[19] It is important to remember that International Shipping Lanes (ISLs) and Sea Lines of Communication (SLOCs) are not interchangeable terms. While the geographical orientation of ISLs is determined by purely economic and navigational-safety considerations, the positioning and geographical orientation of SLOCs is determined by military-operational considerations.

[20] Rishi Iyengar, and John Defterios, “India is Buying More US and Saudi oil because of Sanctions on Iran”, https://edition.cnn.com/2019/06/26/business/indian-oil-us-iran-sanctions/index.html

[21] United Nations, “Climate Change”, https://www.un.org/en/sections/issues-depth/climate-change/

[22] The National Aeronautics and Space Administration (NASA), “Sea Level”, https://climate.nasa.gov/vital-signs/sea-level/

[23] National Oceanic and Atmospheric Administration (NOAA), “What is Ocean Acidification?” https://www.pmel.noaa.gov/co2/story/What+is+Ocean+Acidification%3F

[24] Intergovernmental Panel on Climate Change (IPCC), “Special Report on Renewable Energy Sources and Climate Change Mitigation”, 2012, https://www.ipcc.ch/site/assets/uploads/2018/03/SRREN_FD_SPM_final-1.pdf

[25]Climate action tracker website. “India summary of pledges and targets.” climateactiontracker.org. https://climateactiontracker.org/countries/india/pledges-and-targets/ (accessed December 2, 2019)

[26]Government of India, Climate Change, Sustainable Development and Energy Report from Economic Survey-2016/17, https://www.indiabudget.gov.in/budget2017-2018/es2016-17/echap05_vol2.pdf

Energy Observer, launched in April 2017, is the first vessel in the world to both generate and be powered by hydrogen, relying on a renewable energy mix for onboard production.

Energy Observer, launched in April 2017, is the first vessel in the world to both generate and be powered by hydrogen, relying on a renewable energy mix for onboard production.  THE NEW YORK TIMES

THE NEW YORK TIMES

The Indian navy Shivalik-class stealth multi-role frigate INS Kamorta (F49) and the Japan Maritime Self-Defense Force Akizuki-class destroyer JS Fuyuzuki (DD 118) underway in formation during exercise Malabar 2018. Malabar is designed to advance military-to-military coordination in a multinational environment between the U.S., Japanese, Indian and now Australian maritime forces. (U.S. Navy photo by Mass Communication Specialist 2nd Class Sarah Myers/Released)

The Indian navy Shivalik-class stealth multi-role frigate INS Kamorta (F49) and the Japan Maritime Self-Defense Force Akizuki-class destroyer JS Fuyuzuki (DD 118) underway in formation during exercise Malabar 2018. Malabar is designed to advance military-to-military coordination in a multinational environment between the U.S., Japanese, Indian and now Australian maritime forces. (U.S. Navy photo by Mass Communication Specialist 2nd Class Sarah Myers/Released) ")

Leave a Reply

Want to join the discussion?Feel free to contribute!