The succeeding paragraphs constitute the second part (Part 2) of a three-part advocacy of the need for India to secure its future energy-security by effecting a transition away from fossil fuels. The three parts, taken in aggregate, seek to provide Indian policy-makers with a compelling set of arguments, to not only support ocean-based renewable energy as an economically viable and ecologogically sustainable option, but to specifically adopt hydrogen-fuel derived from the oceans as India’s best option.

Part 1 of this advocacy brought out the components of India’s primary-energy basket and the geopolitical vulnerabilities arising from India’s need to import a substantial proportion of these, particularly crude-oil from West Asia. It is important to remember that significant amounts of India’s imports of crude-oil natural gas, which are sourced from beyond West Asia (Nigeria, for example, is a major source), also face large geopolitical vulnerabilities. The ships carrying these imports must transit two major chokepoints, namely the Suez Canal (to enter the Red Sea) and the Strait of Bab-el-Mandeb located at the southern end of the Red Sea. Alternatively, this oil-and-gas bearing shipping must come around the Cape of Good Hope, which is a weather-determined chokepoint. Ships must remain within thirty-odd nautical miles of South Africa’s southern coast so as to ensure navigational safety from the tumultous seas that are encountered at greater distances from the land. Geopolitics, therefore, impacts the security of all of India’s energy-bearing shipping as it travels along the world’s International Shipping Lanes (ISLs). When strategic or operational risk so dictates, India might have to re-route its inbound energy-bearing shipping and instead of moving it along the ISLs, it might choose to move it along dynamically-determined Sea Lines of Communication (SLOCs).[1]

Once they reach their ports-of-destination in India, these imports of energy are merged with indigenous stocks and must now be converted into secondary sources of energy. Thus, the crude-oil is refined into a variety of products (e.g., fuel-oil, diesel, petrol, kerosene, etc.) which might then be used to propel various forms of land-based, airborne, or seaborne platforms, or be converted into electricity. In fact, outside of the transport sector (and some other major ones such as the fertilizer sector, wherein natural gas is used as a major form of feedstock), the vast bulk of India’s primary energy (whether indigenous or imported) is used to generate electricity. This electricity is fed into the country’s electricity (power) grids. There is a second source of electricity-generation which is fed directly by sources such as diesel generators, domestic solar panels, micro-windmills, and so forth. The electricity that is generated in this way does not get distributed via an electricity grid but is consumed pretty-much where it is generated. This sort of electrical generation is, of course, known as ‘off-grid’ power.[2]

Installed Capacity of Electricity-Generation

Figure 1 depicts the the installed capacity of electricity production in India, as of April 30, 2020.[3] As may be seen, the current contribution of renewables (solar, wind, bio power and small hydro power) to the production of electricity in India is 87027.68 MW (87.027 GW). In terms of percentage contribution the figure stands at 23.51%. By including contributions from nuclear power and hydroelectric power, the overall contribution of renewables in percentage terms is 37.68%.

|

|

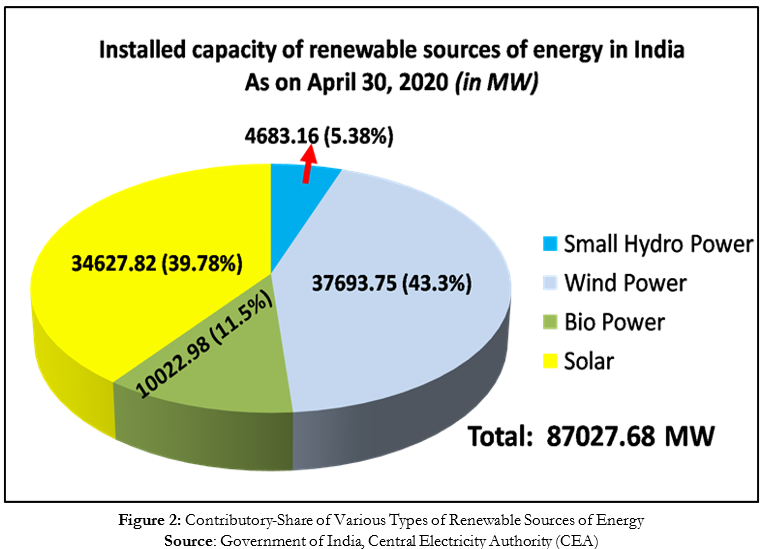

Figure 2, on the other hand, indicates the individual contributions from various sources of renewable power. It is evident that amongst renewables, solar- and wind-energy make-up the lion’s share of the contribution.[4]

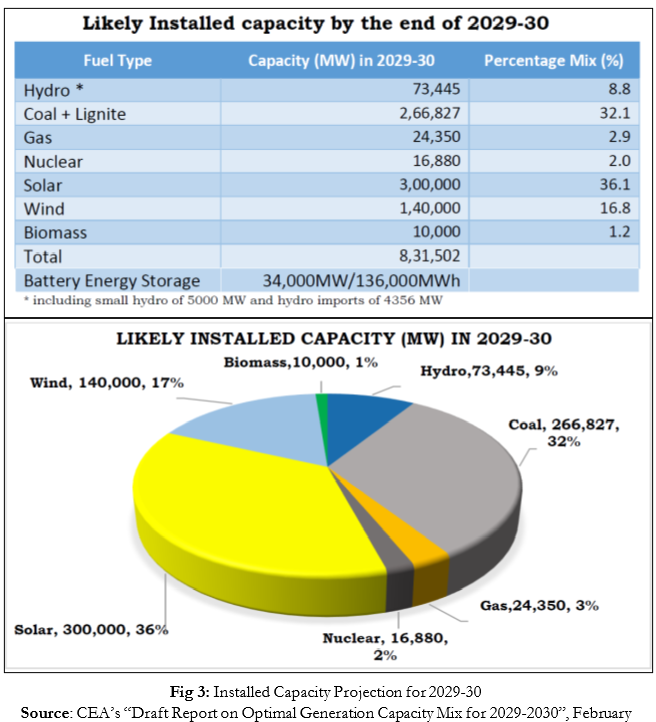

One of India’s three major commitments at the 2015 Paris Agreement,[5] as embodied in the country’s ‘Intended Nationally Determined Contribution’ (INDC), is for 40% of its installed capacity to be from non-fossil sources by the year 2030.[6] New Delhi’s commitment to its energy transition is genuine and its progress toward not merely meeting but exceeding this target is widely acknowledged.[7] Exercising commendable global vision and leadership, India, along with France, established the International Solar Alliance — a multilateral organisation, headquartered in the Delhi NCR, which promotes the adoption of solar energy.[8] Advancing Prime Minister Narendra Modi’s vision to effect India’s speedy transition to renewable resources for the production of electricity, the Central Electricity Authority (CEA) has, in its Draft Report (of February, 2019) on “Optimal Generation Capacity Mix for 2029-2030”, projected that “renewable energy sources (solar + wind) installed capacity will become 440 GW by the end of year 2029-30, which is more than 50% of total [projected] installed capacity of 831 GW”.[9] India’s likely installed capacity by the end of 2029-30 is tabulated and graphically depicted in Figure 3.[10]

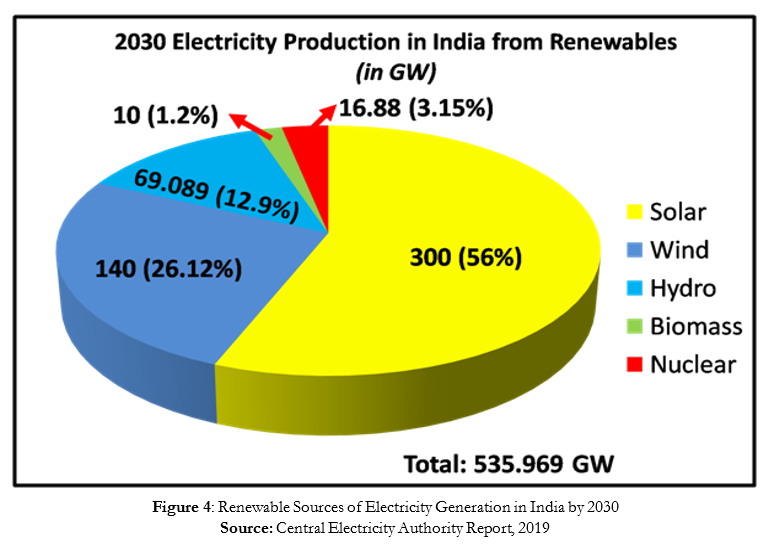

It is also encouraging that India’s dependence upon fossil fuels for electricity-production, in terms of absolute capacity added per annum, is declining and yielding a greater share to renewable resources of energy.[11] Figure 4 depicts the breakdown of the various forms of renewable energy which, according the the CEA’s projection, will feed into the country’s installed-capacity by the year 2030. It is envisioned that around 535 GW (close to 65%) of electricity will be generated from renewables out of the total installed capacity of 831 GW by the year 2030.[12]

|

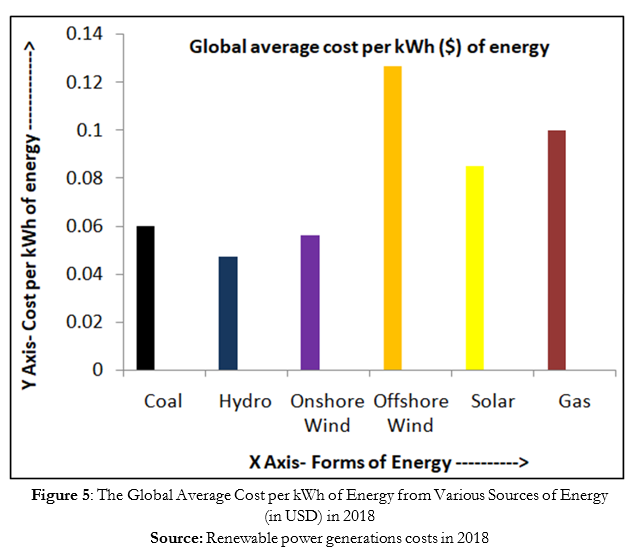

In considering sources of electricity generation, a very important factor is economic viabilty, as established by the cost per kilowatt-hour of electricity generated if the energy-source in question were to be used. This is particularly germane in India, which is the cheapest in the entire Indo-Pacific region and in which the margins between one and another source of electricity-generation is cutthroat. Technologies for the production of renewable energy, such as solar energy and wind energy, as also the development of their respective markets, have attained maturity, with electricity-costs being comparable to that for electricity generated through fossil-fuels. As of 2018, the cost per kilowatthour (kWh) of energy from fossil fuels, compared to solar and wind energy is given in the bar chart in Figure 5. The global average cost of solar-generated electricity was $0.085 or ₹6.47 per kWh, displaying a reduction of 13% from the previous year. In the case of electricity generated from offshore wind, it is $0.127 or ₹9.67, displaying dip of 1% compared to the previous year.[13]

This downward trend is continuing and nowhere as rapidly as in India, where by the end of 2019, the “levelised cost of electricity generation from fossil fuel [was] around $44.5 per MWh (Rs 3.05 per unit)…” while the “levelised cost of solar power generation [was] estimated at around $38.2 MWh (Rs 2.62 per unit)...”[14]

In September 2019, Prime Minister Modi announced that India would add 450 GW of electricity-generation capacity, exclusively from renewables, by the year 2030.[15] It is vital to explore various sources of renewable energy to enable this transition, keeping in mind the fact that India’s demand for electricity is set to increase threefold by the year 2040.[16] This requires a concerted effort, especially considering the current share of renewables in India is currently only 87 GW (Figure 2 refers). Improving the share of renewables would not only reduce carbon emissions but would also play a major role in reducing India’s dependence on energy-imports per se. Therefore, exploring and exploiting every form of available renewable energy in India is an inescapable necessity. The projections by the CEA in terms of installed capacity and the share of various forms of energy, especially renewable forms energy, to this installed capacity are extremely encouraging — but only if the government’s projections are correct. The question, of course, is whether this is really the case.

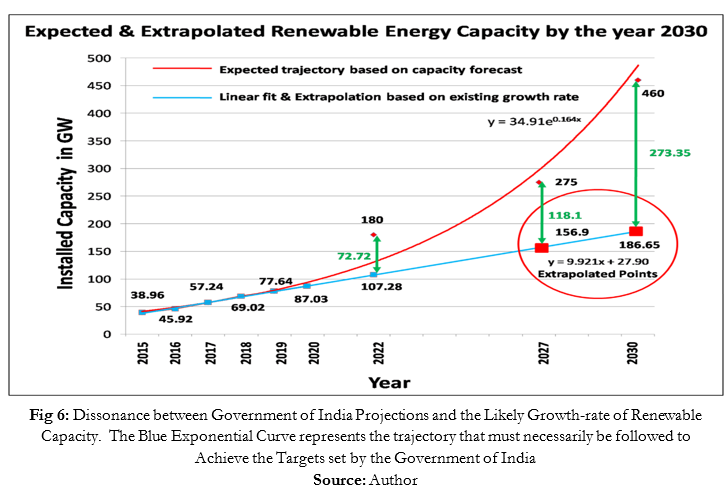

Unfortunately, trend-analysis in terms of the contribution of renewables, undertaken by this author, does not bear out the CEA’s optimism and yields a much grimmer picture that brings the credibility of the CEA’s projections into some doubt. Figure 6 demonstrates, in blue, a ‘linear’ growth-rate of capacity-addition of renewable sources of energy over the last six years, which has been extrapolated for the years 2027 and 2030, so as to enable a comparison with Government of India projections for these years, which are available and have already been referred-to in this paper. The exponential curve, on the other hand, which is depicted in red, represents the trajectory that India will have to follow if it is to actually achieve the targets to which the Government of India has committed itself.

|

The growth-rate of renewable capacity-addition per annum has followed a linear trend over the last six years, with an average growth rate of 9.6 GW per annum. A linear extrapolation, based on the existing trend in growth-rate has been carried out in order to estimate the total renewable installed-capacities by the years 2027 and 2030. This yields figures of 156.9 GW and 186.65 GW, respectively, which fall far short of the ambitious projections of the CEA, which are 275 GW and 460 GW, respectively, for the two years under reference. In fact, in order to achieve these projected-targets, the growth rate from here onward should assume an exponential trajectory (~5.73*exp [0.164x]). This discrepancy is demonstrated in Figure 6, where the Blue line represents the linear growth rate over the last six years and is extrapolated for the years 2027 & 2030. The Red curve represents the exponential trajectory that needs to be followed in order to achieve the capacity-addition targets that have been projected by the CEA for 2027 and those subsequently projected for 2030. The deviation from the projected targets (shown in Green in Figure 6) is already evident by the year 2022, where the existing ‘linear’ trend yields a figure of a mere 107.28 GW as opposed to the projected (and hence ‘targeted’) capacity of 180 GW.

What this means is that the existing mix of renewable sources of energy will not take India to its declared targets. Some other source(s) will have to be identified. This is where Ocean Renewable Energy Resources (ORER) and hydrogen-fuel from the sea enter the picture.

Before proceeding any further in this ongoing advocacy for the adoption by India of hydrogen-fuel as the most promising ORER, there is one very important aspect that needs to be continuously borne in mind — maritime geopolitics.

For this geopolitical maritime piece to be correctly positioned in the reader’s mind, it is critical to remember that electricity-generation alone does NOT constitute the entire Indian energy story. The transport sector (comprising surface-, airborne-, and seaborne transport) still largely relies on crude-oil imports and their refinement into petroleum-products. 98% of energy for transportation is met using diesel, gasoline, natural gas and aviation fuel, as depicted in Figure 7.[17] If this return to petroleum-based import-dependence were not bad enough, the contribution of road-vehicles to air-pollution has significantly affected the Air Quality Index (AQI) in Indian cities, which figure prominently amongst the most polluted cities in the world.[18] According to a joint report by Greenpeace Southeast Asia, and the Center for Research on Energy and Clean Air, the estimated cost of air-pollution in India stands at a whopping $150 billion (close to 5% of India’s GDP) and leads to the premature death of at the least a million people in India per year from pollution-related ailments.[19]

It may thus be seen that in the Indian context, a transition away from fossil fuels and in favour of renewables has to occur simultaneously not only in the generation of electricity but also in the transport sector. This is a major challenge unless the problem of electricity storage can be solved, because “In 2018, around 70 gigawatt-hours (GWh) of battery cells were used for electric cars worldwide, while 8 GWh of stationary batteries were added to provide flexibility in the power sector…”[20] and insofar as the transport sector is concerned, “India is going to need more battery storage than any other country for its ambitious renewables push”.[21] Encouragingly, advances in technology are proceeding at a pace that can only be described as frenetic. Consequently, “battery costs have fallen by over 80% since 2010”.[22]

All this notwithstanding, however, for India, as for much of the world, the problem centres upon the availability of cobalt. Despite “a two-decade evolution in battery technology and increasing energy density from nickel-cadmium to nickel-metal hydride and to today’s lithium-ion” batteries, a critical ingredient for the cathodes batteries used by all electrically-driven vehicles (EVs) continues to be cobalt, which constitutes 5% to 30% of the cathodic material.[23] “A typical smart phone battery requires only 5 to 20 grams of cobalt, whereas an EV requires between 4 and 30 kg.” Since cobalt is in extremely short supply in India but abundant in the Demcratic Republic of Congo, the geopolitical implications of India’s desire to switch to EVs are obvious. This is a fact that ought not be lost sight of. Part 1 of this three-part advocacy focused attention on the geopolitics of West Asia and its impact upon India’s import of petroleum-based energy (crude-oil and natural gas). In an effort to mitigate this dependence (quite apart from the environmental aspects), India is seeking to switch to EVs. This makes new, but equally critical geographic areas the focus of the geostrategies that drive India’s geoeconomics and hence shape its geopolitics.

To be continued in Part 3…

*Sameer Guduru, PhD, is an Associate Fellow at the National Maritime Foundation. His research focusses upon technical issues relevant to India’s maritime domain. Part 1 of this ongoing advocacy of his was published on the NMF Website on 12 May 2020 and may be read at https://maritimeindia.org/adoption-by-india-of-hydrogen-an-ocean-renewable-energy-approach-part-1/ . The views expressed by Sameer Guduru are his own and do not necessarily reflect the official stance of the NMF on the issues covered by the author. He can be contacted at associatefellow3.nmf@gmail.com

Endnotes

[1] It is reiterated that International Shipping Lanes (ISLs) and Sea Lines of Communication (SLOCs) are not always interchangeable terms. While the geographical orientation of ISLs is determined by purely economic and navigational-safety considerations, the positioning and geographical orientation of SLOCs is determined by military-operational risk-based considerations.

[2] United States Department of Energy. Off-Grid or Stand-Alone Renewable Energy Systems. https://www.energy.gov/energysaver/grid-or-stand-alone-renewable-energy-systems (accessed May 19, 2020)

[3] Central Electricity Authority, 2020, “All India Installed Capacity (in MW) of Power Stations as on 30 April 2020” http://www.cea.nic.in/reports/monthly/installedcapacity/2020/installed_capacity-04.pdf

[4] Ibid

[5] Natural Resources Defense Council (NRDC) Issue Brief, “The Paris Agreement on Climate Change”, NRDC, 01 November 2017, https://assets.nrdc.org/sites/default/files/paris-agreement-climate-change-2017-ib.pdf

[6] United Nations Framework Convention on Climate Change, “India’s Intended Nationally Determined Contribution: Working Towards Climate Justice”, https://www4.unfccc.int/sites/ndcstaging/PublishedDocuments/India%20First/INDIA%20INDC%20TO%20UNFCCC.pdf

[7] Madhura Joshi, “Transitioning India’s Economy to Clean Energy”, Anjali Jaiswal’s Expert Blog, Natural Resources Defense Council (NRDC), 05 November, 2019, https://www.nrdc.org/experts/anjali-jaiswal/transitioning-indias-economy-clean-energy

[8] International Solar Alliance. https://isolaralliance.org/

[9] Government of India, Ministry of Power, Central Electricity Authority (CEA), “Draft Report on Optimal Generation Capacity Mix for 2029-2030”, February, 2019, http://cea.nic.in/reports/others/planning/irp/Optimal_generation_mix_report.pdf

[10] Ibid

[11] International Energy Agency, “India 2020: Energy Policy Review”, 2020 https://webstore.iea.org/download/direct/2933?fileName=India_2020-Policy_Energy_Review.pdf

[12] Central Electricity Authority, “Draft Report on Optimal Generation Capacity Mix for 2029-30”, 2019. http://cea.nic.in/reports/others/planning/irp/Optimal_generation_mix_report.pdf

[13] International Renewable Energy Agency (IRENA). 2019. Renewable power generations costs in 2018. https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/May/IRENA_Renewable-Power-Generations-Costs-in-2018.pdf

[14] Debjoy Sengupta, “India is APAC’s Cheapest Power Producer”, The Economic Times, 19 August 2019 https://economictimes.indiatimes.com/industry/energy/power/india-is-apacs-cheapest-power-producer/articleshow/70735458.cms?from=mdr

[15] Press Trust of India. “PM Modi vows to more than double India’s non-fossil fuel target to 450 GW.” https://www.indiatoday.in/india/story/pm-modi-vows-more-double-india-non-fossil-fuel-target-450-gw-1602422-2019-09-24 (accessed September 24, 2019)

[16] Nitin Kabeer, “Electricity Demand in India Will Almost Triple Between 2018 and 2040: World Bank”, MERCOM India (Grid, Market & Policy), MERCOM, 24 December 2018, https://mercomindia.com/electricity-demand-india-triple-2018-2040/

[17] International Energy Agency, “India 2020 Energy Policy Review”, 2020. https://webstore.iea.org/download/direct/2933?fileName=India_2020-Policy_Energy_Review.pdf

[18] Broom, Douglas. “6 of the world’s 10 most polluted cities are in India. “https://www.weforum.org/agenda/2020/03/6-of-the-world-s-10-most-polluted-cities-are-in-india/ (accessed March 5, 2020)

[19] Greenpeace Southeast Asia. “Air pollution from fossil fuels costs the world US $8 billion every day: Greenpeace.” https://www.greenpeace.org/southeastasia/press/3586/air-pollution-from-fossil-fuels-costs-the-world-us8-billion-every-day-greenpeace/ (accessed February 12, 2020)

[20] Claudia Pavarini, “India is Going to Need More Battery Storage Than Any Other Country for its Ambitious Renewables Push”, IEA Commentary, 23 January 2020, https://www.iea.org/commentaries/india-is-going-to-need-more-battery-storage-than-any-other-country-for-its-ambitious-renewables-push

[21] Ibid

[22] Ibid

[23] Robin Goad, “New Cobalt Supply Central to Growing Electric Vehicle Market”, Canadian Mining Journal Commentary, 02 January 2019, https://s1.q4cdn.com/337451660/files/doc_downloads/in-the-media/190101-Canadian-Mining-Journal-Cobalt-Commentary.pdf

Energy Observer, launched in April 2017, is the first vessel in the world to both generate and be powered by hydrogen, relying on a renewable energy mix for onboard production.

Energy Observer, launched in April 2017, is the first vessel in the world to both generate and be powered by hydrogen, relying on a renewable energy mix for onboard production. ")

Image Credits: DNA India

Image Credits: DNA India

EASTERN FLEET, INDIAN NAVY

EASTERN FLEET, INDIAN NAVY

Leave a Reply

Want to join the discussion?Feel free to contribute!