https://aumund.com/en/editorials/samson-ship-loading-solutions-for-copper-concentrate-in-latin-america/

https://aumund.com/en/editorials/samson-ship-loading-solutions-for-copper-concentrate-in-latin-america/Mineral resources underpin industrial economies and technological progress and are indispensable to the energy transition, enabling the production of solar panels, wind turbines, and battery storage technologies. Some of these mineral resources have been officially classified as ‘critical’ not only due to their role in the economic development and national security of the country but also because of the potential for disruption in their supply due to their concentrated existence in raw or processed form.[1] India — particularly the Ministry of Mines, identified a list of thirty (30) minerals as ‘critical’ for India utilising broadly the factors of 1) economic importance, 2) supply risk, and 3) minerals identified by individual ministries as critical to their sectors.[2] This included fourteen (14) elements that have both ‘high’ economic importance as well as ‘high’ supply risk, of which for ten (10) minerals including lithium, cobalt, nickel, and some rare earth elements, India is 100% import-dependent. To ensure, “a long-term sustainable supply of critical minerals and strengthen India’s critical mineral value chains”, the Union Government launched the National Critical Mineral Mission in January 2025.[3] While ‘acquisition of critical mineral assets abroad’ and entering into ‘Critical Minerals Partnership Agreements’ with resource-endowed nations have been identified as measures to support long-term sustainable supply, a critical component of the supply chain i.e., the seaborne transportation of those critical minerals, remains a gap in the focus of the Critical Mineral Mission.

The aim of this article is to highlight the importance of the maritime domain to the resilient supply chains of critical minerals. It is particularly directed at the Ministry of Mines (MoM), the Ministry of Ports, Shipping and Waterways (MoPSW), the National Security Council Secretariat (NSCS), and the Indian Navy (IN), and seeks to establish that maritime considerations, including security of critical mineral trade, and efficiency of maritime logistics need to be taken into account when framing policy options for critical mineral supply chains. This article also seeks to highlight that such an assessment needs to be taken for each critical mineral individually as the manner and mode of their shipping and port-handling would differ. This article is the first of a series and lays the groundwork and the rationale for further analysis. Subsequent articles would, thereafter, focus on individual minerals beginning with cobalt, lithium, nickel, copper, graphite, and rare earth elements as they remain the focus of current policy efforts.

The Importance of Seaborne Trade to the Critical Mineral Supply Chain

Seaborne trade supports the entire supply chain of critical minerals from resource-rich nations to processing hubs to the end-user as most of these minerals — in raw, semi-processed, or processed form — are shipped across the oceans.[4] As per the United Nations Conference on Trade and Development (UNCTAD), critical minerals (as classified by UNCTAD) accounted for 31 percent of global shipping volumes in 2023.[5] This is a consequence of the geographical distribution of the occurrence of the resource mineral as well their refining/processing capacities. This makes the supply chain of these minerals inherently globalised (albeit highly concentrated) and reliance upon seaborne trade is a natural consequence. Therefore, changes-to, impacts-upon, and efficiencies-in the maritime logistics of critical minerals will have an impact on the supply chain and consequently on the availability of critical minerals. The correlation between national critical mineral policies and international shipping patterns can be demonstrated by the changes in volumes of shipped raw cobalt ore vis-à-vis semi-processed intermediate products.

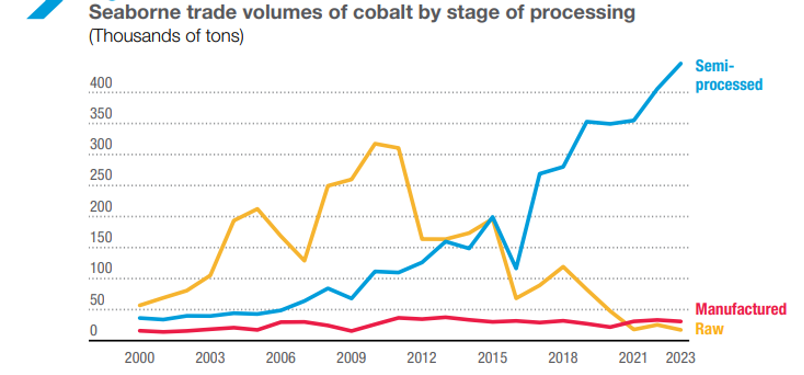

Fig 1: Seaborne trade volumes of cobalt by stage of processing

Source: UNCTAD, Review of Maritime Transport 2025

As may be seen in Fig 1,[6] around 2015-16, there was a significant surge in the shipped volume of semi-processed cobalt. This was a consequence of policy incentives of value-addition within major producing nations, export restrictions in jurisdictions of raw ore and mandatory downstream value-addition, increasing international investment in local refining capacities, and cost efficiency of supply chain integration of upstream and downstream industries.[7] It led to a greater requirement to ship semi-processed products (as opposed to raw ore) and there was a shift in shipping trends associated with such products. The transportation of raw ore is often done loose (through bulk carriers) while processed intermediate or final products, which require stricter safety measures, are shipped in containers which allow for safer handling.[8] Therefore, policies on critical minerals and policies on maritime infrastructure need to move in a coordinated fashion. The following aspects need to be considered when assessing the maritime impacts on the supply chain of critical raw minerals:

Physical Security. The disruption of the maritime traffic carrying these goods is a part of the ‘supply risk’ of these minerals. While it is true that such risk is posed to the maritime transport of all goods, the economic importance and the ‘critical’ classification of these minerals justifies the attention of Indian policymakers to their transportation, quite similar to the focus placed on the security of energy resources. Therefore, policy initiatives by India on supply chain resilience of critical minerals, either through direct acquisition of mineral assets or trade needs to include initiatives on resilient seaborne transportation. It is important to track the routes through which specific ‘critical’ minerals reach India, so as to anticipate, prepare, protect, and insure against any threats. Since the occurrence of the resource and their processing facilities differ for each mineral, an individual assessment needs to be taken for each mineral and their associated maritime supply chains. This assessment also remains dynamic as India seeks to conclude critical mineral partnerships to diversify supply chains, including the conclusion of deals with Canada, Brazil, and France, all of which will also open new critical mineral shipping routes.[9]

Freight, Shipping and Insurance Costs. A well-known impact of geopolitical risks and the security of maritime trade is the impact on freight capacity, freight charges, bunkering costs, and insurance premiums on shipping.[10] The Baltic Dry Index (BDI) — an oft-used indicator measuring international dry-bulk shipping costs for Capesize, Panamax, and Supramax bulk carriers — is linked to oil price fluctuations and dependent on global economic and business conditions, which in turn are subject to geopolitical risk.[11] A study modelling the impact of geopolitical risk on the freight rates of Capesize and Panamax dry-bulk carriers (which are predominantly used to transport mineral ore) demonstrated that geopolitical risks can significantly increase freight rates taking up to twenty months to fully recover from the shock.[12] In 2024, the Red Sea crisis significantly drove up spot container freight rates which intersect with the routes for India-bound critical minerals processed and/or refined in Europe.[13] The implications of the increases in freight and charter charges on select routes owing to geopolitical causes needs to be factored, especially for investments made towards the acquiring of assets abroad. So, while Khanij Bidesh India Ltd (KABIL) has signed a US$ 24 million pact to explore five (05) lithium brine blocks in Argentina, there is no clarity yet as to what KABIL plans to do with the lithium ore once production commences.[14] It is possible that the Government of India decides to either process it within Argentina itself, and ship semi-processed lithium to India. It is possible that it decides to ship the ore for processing and refinement to another partner country, and/or import the raw ore for refinement and processing in India (assuming that India develops the required indigenous capacity and capability). In each scenario, the availability and cost of shipping will be a major factor in the economic viability of the endeavour which is extremely important for its long-term sustainability.

Efficiency of Maritime Logistics. It must be noted that the issue of seaborne transportation of critical minerals is necessary not only in the context of security from external threats but also for the development of efficiencies within maritime logistics. This includes aspects such as port infrastructure (the capacity and capability of ports in to handle critical mineral cargo in its raw and/or processed form), the availability of requisite shipping capacity to transport those critical minerals — again in raw and/or processed form, and efficient trade facilitation systems.

While the impact of maritime logistics on the success of policy-efforts within the National Critical Mineral Mission involving acquisition of assets abroad to supply critical minerals to India is more discernible, strengthening India’s mineral value chains is greatly dependent upon robust maritime logistics. Investment in mid-stream/downstream mineral processing facilities may well be made, but economies of scale can only be achieved with a stable, consistent, and efficient supply of raw ore. Much of the critical minerals imported into India currently are in semi-processed or processed form.[15] As mentioned earlier, the transportation of raw ore is often done loose through bulk carriers while processed intermediate or final products are shipped in containers.[16] While such an increase in the quantity of import of raw ore would, of course, require the availability of a greater number of bulk carriers and the appropriate bulk cargo handling facilities at ports, these are not major challenges, particularly in environmental conditions of peace and stability. However, the Indian Navy and the MoPSW at the very least, need to jointly discuss and formulate plans that would assure the safe transportation of these critical minerals in times of tension and conflict. Should the ships that are engaged in their transport be restricted to those flying the Indian flag? Will specific sea lines of communication (SLOCs) need to be devised — as opposed to the normal international shipping lanes (ISLs) that are used in times of peace? Will such ships be routed independently? Escorted by warships? Convoyed?

In 2016, the MoPSW released a “Berthing Policy for Dry Bulk Cargo for Major Ports” as it had identified that dry bulk commodity handling suffered from low productivity, leading to high turn-around times and higher berth-occupancy rates — a challenge that is likely to compound over time, considering future growth.[17] The policy identified that productivity level of unloading operations of dry bulk cargo (in tonnes of cargo unloaded per berth per day) was a function of the density of the commodity, the size of the crane-grab available, picking factor for the particular commodity, number of cycles per hour (itself a function of the type and size of crane and stage of operation), and vessel profile, among other things. Therefore, maintaining high productivity is squarely dependent upon the available grab equipment being suitable for the material that is sought to be evacuated (the grab size of the crane and density of the material affect the quantity of material per lift and consequently total quantity of material evacuated in a given day). The policy goes further to identify the optimum grab-size for different commodity-to-crane combinations and sets an incentive/disincentive structure by computing performance norms for specific products. Penalties in berthing charges will have to paid for a vessel exceeding the time spent on berth than that stipulated for the size of the vessel and commodity(ies) it is carrying. Therefore, each commodity would have to be independently accounted-for with respect to its density, and identified ports would need to be equipped with the appropriate size and number of cranes to cater for effective evacuation of any future raw ore planned to be imported into India. A broader level of concern is that if the quantum of critical mineral ore increases significantly in any given port that handles dry-bulk cargo, this could create a competition between the existing types of dry-bulk (currently dominated by coal and iron ore) being handled by the port, and the new arrivals of critical-mineral ore (insofar as handling-capacity of the port, the cargo dwell time, and the cargo evacuation rate, are concerned). This is true of major ports as well as non-major ones. For instance, in FY 2024-25, non-major ports in India, such as Dhamra (45 MMT), Dahej (14 MMTPA with two dry bulk berths), Mundra, and Pipavav (4-5 MMT) handle significant dry bulk cargo but their operations are currently focused upon coal.[18] Clearly, more granular analysis will be required to determine the spare capacity available in each such port to efficiently absorb any increase in imports of raw ore or whether existing coal trade would have to be diverted to alternative ports and if so, these would need to be specifically identified.

Such analysis also needs to be undertaken for containerised shipping of semi-processed minerals, especially given that some intermediate mineral products are classified as hazardous or dangerous goods and require special handling procedures. For instance, cobalt Di hydroxide — one of the main cobalt compounds imported into India — is placed within Class 6.1 (Toxic Substances) and Packing Group I (High Danger), of the Dangerous Goods List, as per Amendment 42-24 to the International Maritime Dangerous Goods (IMDG) Code binding upon all flags party to the International Convention for the Safety of Life at Sea 1974 (SOLAS).[19] Radioisotopes of cobalt such as Co-57 and Co-60, and some Rare Earth Elements, are placed in Class 7 with specified transport security thresholds on quantity above which they are identified as “high consequence radioactive material” and have special security and transportation requirements. As per the Code, companies, ships, and port facilities need to adopt training measures for offshore and shore-side crew, a security plan, and adhere to strict packaging, segregation, labelling, and at times even quantity restrictions. For instance, Jawaharlal Nehru Port Regulations, 2007, specify safety procedures for “Dangerous Goods (Arrival, Receipt, Transport, Handling and Storage)”, which seek to give effect to international conventions governing the transport of dangerous goods at sea, and their handling in the port.

At this stage, this article seeks only to sensitise policymakers to the fact that these factors are important when making policy decisions about long term investments in ore production, processing, and refinement. Once India has acquired raw ore from a foreign asset where should she process it? What stage of processing/refinement should happen in India or in another partner country? Should different compounds be processed in different places? Where does the ore and or processed / refined compound land in India? It is possible that only a few ports in India have the capacity and capability to handle and store such cargo safely. A critical component of the answer to these questions will lie in the feasibility and cost-effectiveness of transportation from origin to destination. These questions are important for policymakers in India to answer (as opposed to a mere private logistics challenge) because the National Critical Minerals Mission identifies public sector entities (including KABIL) to undertake such investments abroad.

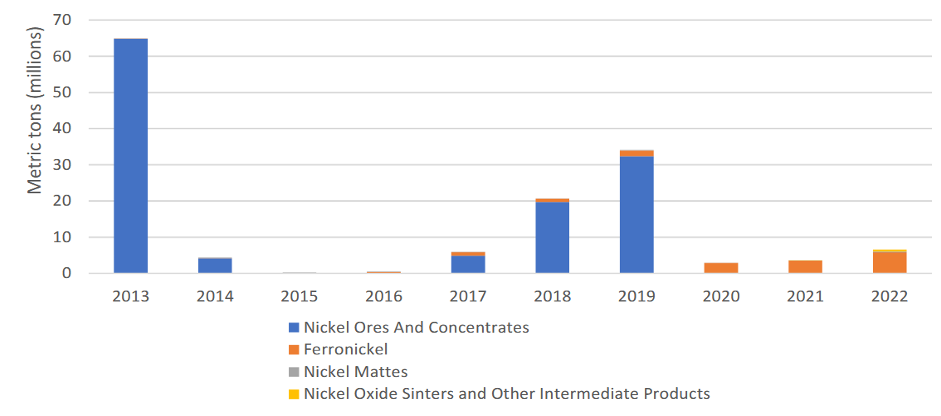

It must be borne in mind that such an analysis will have to factor the assessed future demand, which is, in and of itself, a function of changes in technology and policy. For instance, given the high supply-chain risk of cobalt for producing nickel-manganese-cobalt batteries to power electric vehicles, cobalt-free alternatives, such as lithium-iron-phosphate batteries are being explored even if they have lower energy density.[20] This is likely to have a bearing on not only the demand for cobalt but also for nickel and iron which would be in greater demand to produce these alternatives. While technological changes are more likely to affect which mineral flows are initiated, changes in policy — especially those of resource-rich nations — will affect the form in which they are transported. In addition to the example cited in Fig 1, the export ban of raw nickel ore from Indonesia — a move undertaken to advance investment in domestic downstream processing facilities, since the unit value of processed goods exports are significantly higher than raw ore — significantly altered the quantity of exports of nickel.[21]

Fig 2: Indonesian Nickel Exports by Quantity (2013-22)

Source: Guberman, Schreiber & Perry, Export Restrictions on Minerals and Metals.

Figure 2 shows that moving from the export or import of ‘raw ore and concentrate’ to ‘processed products’ has a significant impact on the quantity that is required to be shipped. This does not necessarily translate into fewer shipments due to the difference in transportation mechanisms between dry bulk carrier and a container ship. The higher densities of processed products may result in the shipment hitting weight limits before volume limits.

The Government of India is, indeed, making and inviting investments in both port infrastructure and ship building initiatives through the SAGARMALA Programme in line with the Maritime India Vision 2030 (MIV 2030) to boost the maritime sector and reduce logistics costs in India. New ports and new investments offer opportunities to incorporate critical minerals in their planning to ensure that the National Critical Minerals Mission moves from policy to implementation. There does, however, need to be greater policy coordination between the MoPSW and the MoM, to ensure that India’s maritime industry is in a position to support India’s efforts to establish long term supply chains and enhance the value chains for critical minerals in India. Given the fact that recent events from Ukraine to the Persian Gulf have demonstrated the fragility and brittleness of the desired environmental condition of peace, it would be imprudent in the extreme to leave the Indian Navy out of this rapidly developing picture.

*******

About the Author:

Mr Soham Agarwal, a Delhi-based lawyer, holds a Bachelor of Law (Honours) degree from the University of Nottingham, UK. He is currently an Associate Fellow with the Public International Maritime Law and Resilience Sustainability and Ocean Resources Cluster of the National Maritime Foundation, New Delhi. His research, which is focused upon issues relevant to the seabed including maritime infrastructure, offshore resources, critical minerals, disaster-resilience, seabed warfare, and ocean governance is rapidly gaining significant traction internationally as well as nationally. He may be contacted at law10.nmf@gmail.com

Endnotes:

[1] Ministry of Mines, Critical Minerals for India: Report of the Committee on Identification of Critical Minerals (New Delhi: Ministry of Mines, June 2023) https://mines.gov.in/admin/download/649d4212cceb01688027666.pdf

[2] Ministry of Mines, Critical Minerals for India

[3] Ministry of Mines, National Critical Mineral Mission 2025 (New Delhi: Ministry of Mines, 2025) https://mines.gov.in/admin/storage/ckeditor/NCMM_1739251643.pdf

[4] United Nations Conference on Trade and Development (UNCTAD), Review of Maritime Transport 2025: Staying the Course in Turbulent Waters (Geneva: United Nations, 2025). https://unctad.org/system/files/official-document/rmt2025_en.pdf

[5] UNCTAD, Review of Maritime Transport 2025.

[6] UNCTAD, Review of Maritime Transport 2025.

[7] International Energy Agency (IEA), Critical Minerals Market Review 2023 (Paris: International Energy Agency, 2023) https://iea.blob.core.windows.net/assets/c7716240-ab4f-4f5d-b138-291e76c6a7c7/CriticalMineralsMarketReview2023.pdf

[8] UNCTAD, Review of Maritime Transport 2025.

[9] Neha Arora, “India Talks Over Critical Minerals Deals with Brazil, Canada, France, Netherlands,” Reuters, 10 February 2026 https://www.reuters.com/world/india/india-talks-over-critical-minerals-deals-with-brazil-canada-france-netherlands-2026-02-10/

[10] Pengjun Zhao and Tong Zhao, “The Relationships between Geopolitics and Global Critical Minerals Shipping: A Literature Review,” Ocean & Coastal Management 262 (March 2025): 107559 https://www.sciencedirect.com/science/article/abs/pii/S0964569125000213?fr=RR-2&ref=pdf_download&rr=9d2cb6833c9124b2

[11] Manuel Monge, María Fátima Romero Rojo, and Luis Alberiko Gil-Alana, “The Impact of Geopolitical Risk on the Behavior of Oil Prices and Freight Rates,” Energy 269 (15 April 2023): 126779 https://www.sciencedirect.com/science/article/pii/S0360544223001731?via%3Dihub#fn1

[12] Wolfgang Drobetz, Konstantinos Gavriilidis, Styliani-Iris Krokida, and Dimitris Tsouknidis, “The Effects of Geopolitical Risk and Economic Policy Uncertainty on Dry Bulk Shipping Freight Rates,” Applied Economics 53, no. 19 (2021): 2218–2229 https://www.tandfonline.com/doi/abs/10.1080/00036846.2020.1857329

[13] https://www.maersk.com/insights/resilience/2024/07/09/effects-of-red-sea-shipping

[14] Manish Poswal, “India’s KABIL Seals $24 Million Lithium Exploration Pact with Argentina,” DD News, 16 January 2024 https://ddnews.gov.in/en/indias-kabil-seals-24-million-lithium-exploration-pact-with-argentina/

[15] Rahul Mazumdar and Dhitika Shah, India’s Need to Secure Critical Minerals for Energy Transition, Occasional Paper No. 230 (Mumbai: Export-Import Bank of India, 2025) https://www.eximbankindia.in/sites/default/files/2025-07/211file%20%281%29.pdf?utm_source=chatgpt.com

[16] UNCTAD, Review of Maritime Transport 2025.

[17] Ministry of Ports, Shipping and Waterways, Berthing Policy for Dry Bulk Cargo for Major Ports (New Delhi: Ministry of Shipping, August 2016) https://shipmin.gov.in/sites/default/files/6379333834berthingpolicydrybulkcargo.pdf

[18] Bureau of Research on Industry and Economic Fundamentals, Impact of Non-Major Ports on Shipping (New Delhi: NITI Aayog, March 2025) https://niti.gov.in/sites/default/files/2025-03/Final%20%20report%20on%20Impact%20of%20Non-Major%20Ports%20on%20%20Shipping.pdf

[19] International Maritime Organization (IMO), Amendments to the International Maritime Dangerous Goods (IMDG) Code: Amendment 42-24 (London: International Maritime Organization, 2024). https://www.register-iri.com/wp-content/uploads/MSC.556108.pdf

[20] Solomon Evro et al, “Navigating Battery Choices: A Comparative Study of Lithium Iron Phosphate and Nickel Manganese Cobalt Battery Technologies,” Future Batteries 4 (December 2024): 100007 https://www.sciencedirect.com/science/article/pii/S2950264024000078

[21] David Guberman, Samantha Schreiber, and Anna Perry, Export Restrictions on Minerals and Metals: Indonesia’s Export Ban of Nickel, Working Paper ICA-104 (Washington, D.C.: Office of Industry and Competitiveness Analysis, U.S. International Trade Commission, February 2024) https://www.usitc.gov/publications/332/working_papers/ermm_indonesia_export_ban_of_nickel.pdf

Leave a Reply

Want to join the discussion?Feel free to contribute!