The impacts of climate change are now affecting the way of life for billions of people in almost every part of the planet. Future projections, derived from the latest climate models, suggest that the global average temperature could rise by as much as 5.6 °C above pre-industrial levels if the carbon dioxide (CO2) concentration in the atmosphere is doubled (this is commonly known as ‘Equilibrium Climate Sensitivity’).[1] The consequences of such a large temperature rise will be catastrophic for human civilisations. In 2015, over 190 countries signed the Paris Agreement[2] and agreed to halt global warming at a threshold well below 2°C, aiming, in fact, for a threshold of 1.5 °C, in order to avoid the worst effects of climate change. In 2018, the United Nations (UN) Intergovernmental Panel on Climate Change (IPCC), in its Special Report on Global Warming of 1.5 °C, stated that in order to limit global warming below 1.5 °C, global human-caused carbon emissions must decline to around half of their 2010 levels by 2030, and reach net zero by 2050.[3] This poses a Herculean challenge, which requires nothing short of urgent and transformative action in all sectors of all economies around the world. This transition is currently being led by the energy sector, through the growth of renewable energy sources such as solar and wind, owing to recent advances in their efficiency and accessibility. However, other, equally-critical sectors of the global economy still require innovative solutions to reduce their carbon emissions. According to 2019 data, 98 per cent of the global transportation sector still runs on fossil fuels.[4] In this context, this article will assess the contribution of the global shipping industry, which forms the backbone of international trade, to global greenhouse-gas emissions. The article will highlight some of the key issues and challenges associated with the quantification and classification of shipping emissions. It will conclude by discussing solutions and mitigation strategies to decarbonise the shipping sector while managing the increasing trade volumes in the future.

Quantifying Shipping Emissions

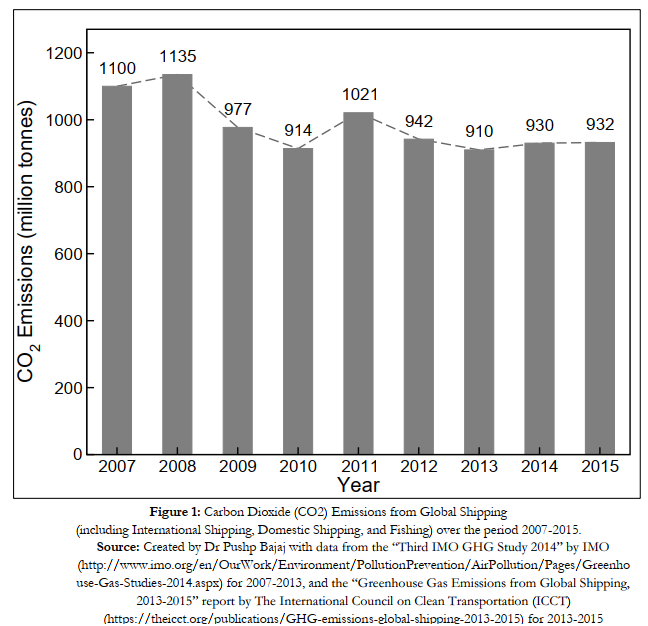

The shipping sector accounts for around 90 per cent of global trade and is the most carbon efficient mode of transportation for goods.[5] However, in terms of absolute numbers it is one of the largest carbon emitting sectors, accounting for 2-3 per cent of the global greenhouse gas (GHG) emissions. If it were a country, it would be the sixth largest GHG emitter in the world, placed between Japan (which is in the fifth position) and Germany (which is in the seventh position). It is estimated that global shipping currently emits 90000 tonnes/hr or 25 tonnes/sec of CO2. It is important to note that GHG emissions from ships are not restricted to the duration of their voyage but also occur while they are berthed alongside or are at anchor in or off seaports and harbours. Moreover, since ships have long lifetimes, spanning two to three decades, these emissions are committed-for for many years in the future.[6] In 2015, carbon emissions from global shipping, including domestic shipping, international shipping, and fishing, were estimated to be 932 million tonnes (see Figure 1).[7] International shipping alone contributed around 812 million tonnes which is 282 million tonnes higher when compared to emissions from international aviation.[8]

Official data maintained by the UN’s International Maritime Organisation (IMO) since 2007 show a reduction in CO2 emissions between 2008 and 2009 followed by a plateau (see Figure 1). The sudden dip in emissions in 2009 could be attributed to the slowdown in trade caused by the global financial crisis (GFC) of 2008.[9] A similar kink can be seen in the activity of the global aviation sector during the same time period, immediately after the GFC. Similarly, with the reduction of maritime activity during the era of the Covid-19 global pandemic, the carbon emissions are likely to plummet from previously estimated values in a ‘business as usual’ (BAU) scenario.[10] The plateau in emissions since 2009, despite consistent growth in seaborne trade, could be explained by the stricter energy efficiency standards imposed by the IMO and the ensuing technological advances in the design of the main engines of merchant ships, leading to a decrease in ‘emissions intensity’.

Official data maintained by the UN’s International Maritime Organisation (IMO) since 2007 show a reduction in CO2 emissions between 2008 and 2009 followed by a plateau (see Figure 1). The sudden dip in emissions in 2009 could be attributed to the slowdown in trade caused by the global financial crisis (GFC) of 2008.[9] A similar kink can be seen in the activity of the global aviation sector during the same time period, immediately after the GFC. Similarly, with the reduction of maritime activity during the era of the Covid-19 global pandemic, the carbon emissions are likely to plummet from previously estimated values in a ‘business as usual’ (BAU) scenario.[10] The plateau in emissions since 2009, despite consistent growth in seaborne trade, could be explained by the stricter energy efficiency standards imposed by the IMO and the ensuing technological advances in the design of the main engines of merchant ships, leading to a decrease in ‘emissions intensity’.

According to the projections made by the IMO, in its “Third IMO GHG Study 2014”[11] by the year 2050, carbon emissions from global shipping are likely to increase by 50-250 per cent, under business-as-usual scenarios, relative to 2012 levels. The large range of predictions is representative of the uncertainties in future oil demand, fuel-efficiency of ships, and the rate of growth of international trade. Clearly, the shipping industry is a major contributor to global GHG emissions and will continue to contribute more and more in the future. Hence, the shipping sector will play a vital role in achieving the global warming targets established in the 2015 Paris Agreement. It is important to remember that the Paris Agreement was signed by ‘countries’ and not ‘private companies’. The question that then arises is: what role can/ should individual nations play in addressing carbon emissions from shipping, which is inherently a complex, interconnected, international sector? In this regard, the complexities and challenges involved in attributing the carbon emissions to individual countries, and the various technological and operational solutions that can be adopted to reduce these emissions, are deliberated-upon in the succeeding paragraphs.

Challenges in Classifying Shipping Emissions

The shipping industry is quite unique in the way its operations are conducted. For instance, it is common for a cargo ship to be owned by one country, fly the flag of a second country, carry cargo belonging to a third country, and be manned by crew from a fourth country. Naturally, this complicates the monitoring and country-wise attribution of GHG emissions from a given ship during a given trip. Present mechanisms do not involve any country-specific data-collection of the emissions that could then be included in the total carbon emissions of individual countries. Understandably, the international nature of the shipping industry demands an international regulatory body. The IMO, in this case, is the principal authority under the aegis of the UN responsible for the daunting tasks of recording, classifying, and regulating global shipping emissions.

Currently, there are two data-collection mechanisms for shipping emissions. The first is the European Union (EU) MRV regulation, which stands for Monitoring, Reporting and Verification of CO2 emissions from maritime transport. Acknowledging the lack of an international agreement regarding international maritime carbon emissions at the time, the European Parliament passed a resolution on 25 April 2015 to set up the MRV system for CO2 emissions from maritime transport.[12] The MRV entered into force in 2015, and requires all ships equal to or larger than 5000 gross tonnes (GT) that intend to enter EU ports to report their fuel-consumption data which is then used to calculate CO2 emissions.[13] According to the EU, 55 per cent of the ships entering into European waters were above 5000 GT and accounted for around 90 per cent of the maritime emissions in 2015.[14]

The second mechanism is the IMO’s Data Collection System (DCS), which derives its legitimacy from the International Convention on Prevention of Pollution from Shipping (MARPOL) provisions that came into force on 01 March 2018. As is the case with the EU MRV, the IMO DCS applies to ships of 5000 GT and above.[15] However, unlike the EU MRV regulation, which only applies to ships entering EU ports, the IMO DCS applies to all ships entering ports, worldwide. Another distinction is that while the EU MRV data is publicly available, the IMO DCS data is kept confidential and is unavailable in the open domain. Nonetheless, it is mandatory for ships to submit their fuel-oil consumption-data to the IMO as per the amendments made in 2016 to Annex VI of MARPOL. Moreover, as per a new regulation, the data on shipping emissions collected by the IMO is made available to all countries that have ratified the updated MARPOL Annex VI, albeit, under conditions of anonymity, and strictly for the purposes of internal analysis.[16] Due to the diverse nature of the stakeholders and the presence of two different regulatory mechanisms, ship operators have to maintain two separate records for the ship’s fuel consumption, which is an additional administrative burden.

The present classifications of the shipping emissions are primarily based on ship-type and/or flag-state. In its 2017 report on “Greenhouse Gas Emissions from Global Shipping, 2013-2015”,[17] the International Council on Clean Transportation provides a decomposition of CO2 emissions by ship type (see Figure 2).

Container ships, bulk carriers, and oil tankers account for 23, 19, and 13 per cent of the emissions, respectively, amounting to a total of 55 per cent.[18] Clearly, how these three ship types are regulated in the future, will determine a large part of the total shipping CO2 emissions. Annex VI of MARPOL explicitly sets limits on emissions of sulphur oxide, nitrogen oxide, and ozone-depleting substances from the ships. However, it does not explicitly mention CO2.[19] In order to address this issue, a new Chapter 4 was later added to the MARPOL Annex VI, with two regulatory mechanisms, viz., the Energy Efficiency Design Index (EEDI) and the Ship Energy Efficiency Management Plan (SEEMP), to specifically target CO2 emissions. These mechanisms seek to reduce the ‘carbon factor’ i.e. the amount of CO2 generated per unit mass of fuel used.[20]

Container ships, bulk carriers, and oil tankers account for 23, 19, and 13 per cent of the emissions, respectively, amounting to a total of 55 per cent.[18] Clearly, how these three ship types are regulated in the future, will determine a large part of the total shipping CO2 emissions. Annex VI of MARPOL explicitly sets limits on emissions of sulphur oxide, nitrogen oxide, and ozone-depleting substances from the ships. However, it does not explicitly mention CO2.[19] In order to address this issue, a new Chapter 4 was later added to the MARPOL Annex VI, with two regulatory mechanisms, viz., the Energy Efficiency Design Index (EEDI) and the Ship Energy Efficiency Management Plan (SEEMP), to specifically target CO2 emissions. These mechanisms seek to reduce the ‘carbon factor’ i.e. the amount of CO2 generated per unit mass of fuel used.[20]

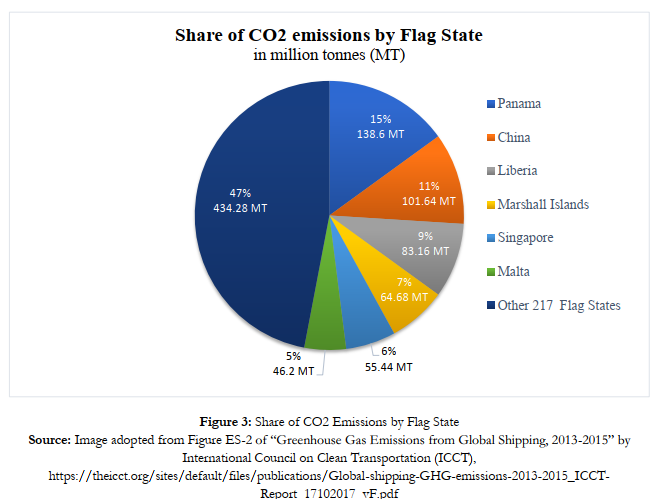

The second commonly used classification of shipping emissions is by flag-state, where just six nations, Panama, China, Liberia, Marshall Islands, Singapore, and Malta (all of which, except for Singapore, have ‘open registries’ wherein ships fly ‘Flags of Convenience’) constitute about 53 per cent of the total CO2 emissions (see Figure 3).

The current legal framework, under the ‘Flag of Convenience’ (FOC) provision, allows ships to register under the flag of any country ‘of convenience’. Very often, shipping companies register their vessels in another country to avoid the stricter regulations and higher financial costs that prevail in the country where the ship has been built, or the country of origin of the owners of the shipping company concerned.[21] Countries such as Panama, Marshall Islands and Liberia make attractive contenders for FOC as they maintain an open registry.[22] The flexible registration and ability to hire cheap foreign labour has resulted in Panama acquiring the largest shipping fleet in the world. It has around 7,100 vessels registered under its flag.[23] This may seem irrelevant to the present discussion until one realises that according to international maritime law, it is the flag state that bears responsibility for the ship’s emissions and for compliance with energy efficiency regulations.

Article 94 of the United Nations Convention on the Law of the Sea (UNCLOS), while defining the duties of a flag-state, stipulates that, “each State is required to conform to generally accepted international regulations, procedures and practices and to take any steps which may be necessary to secure their observance”.[24] It implicitly assigns flag-states with overall responsibility for enforcing and implementing international maritime regulations. As mentioned above, barring China, the majority of the vessels are registered in smaller, less-developed nations such as Panama, Liberia, and Marshall Islands. These nations have neither the financial nor the technological capacity to implement any meaningful solutions to mitigate the rising carbon emissions from ships. Therefore, a flag-state-based classification hides the true identity of the shipowners and stakeholders, and puts the onus on less-equipped nations.

On the other hand, an analysis of annual maritime trade statistics paints a very different picture. Figure 4 depicts the distribution of global seaborne trade in 2018 in terms of goods loaded and unloaded.

Clearly, Asia accounts for the largest amount of trade by a big margin, followed by Europe. Further, looking at individual countries, Figure 5 shows the distribution of the world’s top 20 exporters and importers of containerised cargo (which forms a majority of maritime trade) based on 2014 data.

China undoubtedly leads the world’s exports by a huge margin, followed by the USA, South Korea and Japan. India ranks ninth in the list. In terms of imports, the USA is the world’s largest importer of containerised cargo, followed by China, Japan, and South Korea. Now, while China does rank second in the list of ‘flag-state’ countries, other major maritime trading powers, notably the USA, Japan, and South Korea, are not among the top six. Also noteworthy is that, Panama, Liberia, Marshall Islands, and Malta, that have large numbers of vessels registered under their flag do not make it to the list of top exporters and importers.

This highlights the imbalance between vessels registered in a given nation and the amount of maritime trade undertaken by the same nation. Such an unequal distribution gives a distorted picture of the countries accountable for the carbon emissions. Therefore, the classification of shipping emissions must go beyond flag-states to a more equitable system that is truly representative of each country’s stakes in the global shipping industry. This is crucial for the planning and efficacy of international efforts to reduce GHG emissions from shipping. The Paris Climate Agreement requires each member nation to declare their Nationally Determined Contributions (NDCs) to reduce GHG emissions. Remarkably, shipping emissions are currently not addressed in any nation’s NDCs.[25] Member States must take responsibility for their share of carbon emissions caused due by the intensity of their respective maritime trade. While the industry resolves these administrative and legal challenges, it must simultaneously devise strategies and adopt technologies to mitigate GHG emissions from shipping.

Current Mitigation Strategies and Path Ahead

In April of 2018, the International Maritime Organization (IMO), through its Marine Environment Protection Committee (MEPC), unveiled the “Initial IMO Strategy on Reduction of GHG Emissions from Ships”.[26] It is encouraging to note that the governments of all 100-plus nations that are members of the IMO agreed to an ambitious target of reducing annual shipping emissions by at least 50 per cent by 2050 relative to 2008 levels. The MEPC, on its part, has highlighted measures such as stricter energy efficiency standards, and, increased investment in clean energy technologies and alternative fuels, through cooperation between public and private stakeholders. Considering the sustained growth in international seaborne trade and the lack of low-carbon fuel alternatives at the moment, the 50 per cent reduction target does, indeed, seem ambitious. However, it is important to note that the latest climate-change projections of the UN Intergovernmental Panel on Climate Change (IPCC) show that in order to stay below 1.5 degrees Celsius of global warming, global carbon emissions must go down to net-zero by 2050. Therefore, barring a dramatic increase in carbon sink capacity to offset the emissions, the IMO’s proposed 50 per cent reduction target by 2050 might well be ambitious, but it is, in and of itself, still not enough to meet the UN IPCC climate goals. Arguably, more ambitious measures could be included in the next revision of the strategy which is due in 2023.

Improving Energy Efficiency

Even prior to the GHG reduction strategy of 2018, the IMO had taken measures to address GHG emissions from ships. In 2011, two important energy efficiency measures were introduced: the Energy Efficiency Design Index (EEDI), and, the Ship Energy Efficiency Management Plan (SEEMP).[27] Both these were further emphasised and increased in scope in the 2018 GHG reduction strategy. The EEDI mandates every new ship put into operation after 01 January of 2013 to follow a strict energy efficiency level (in terms of grams of carbon dioxide/capacity-mile), depending on the ship type and size, as defined by the MEPC. Additionally, the reference efficiency standard was set to be tightened incrementally every five years. The SEEMP, on the other hand, provides operational guidelines to improve the efficiency of both, new and existing ships. As per this regulation, each ship must devise, disseminate and execute its own SEEMP, based on the specific ship-type. This individual-ship plan needs to include, inter alia, guidelines for speed optimisation, trim and draught optimisation, just-in-time arrivals at ports, etc. While improved energy-efficiency standards and regulations are necessary and will help in reducing shipping emissions to some extent, the fact remains that without economically viable and readily accessible ‘clean’ alternatives to fossil fuels, we cannot hope to achieve the UN IMO target.

In this regard, several options are being explored by engine manufacturers, scientists, and experts. While the road-transportation sector has quite successfully incorporated electric vehicles including cars and even trucks, a similar transition to electric-vessels in shipping remains an outstanding challenge.

Onshore Power Supply

Carbon emission from ships is not restricted to the period during which the ship is actually sailing (on passage). Even while ships are berthed alongside on jetties, quays and wharves in ports, they contribute to the overall pollution in coastal cities. Auxiliary engines continue to run so as drive motors to power cargo loading and unloading as well as to sustain day-to-day activities on board, as also to cater for mandatory safety-lighting, and a large variety of pumps. The 61st meeting of the MEPC, which was held in 2010, focussed upon ways and means of reducing greenhouse gas emissions from ships in ports and harbours.[28] The delegates identified “On-shore Power Supply” (OPS) or “Cold Ironing” as a viable measure to improve air-quality in ports and port cities by reducing carbon dioxide emissions by ships alongside. This involves replacing onboard generated power from diesel auxiliary engines with electricity supplied by the port.[29]

Ancillary Battery Storage

Currently, batteries and hybrid technologies are being used only for small ships and over short voyages. We are yet to develop large enough batteries at low enough costs that can be used in large cargo ships on longer passages. In addition to these limitations in storage-capacity there are other technical, environmental, and safety challenges involved in creating batteries for large ships. Manufacturing batteries of the size required for ships would require large amounts of Rare Earths (within the Periodic Table, these comprise the fifteen lanthanides, as well as scandium and yttrium), and critical raw materials such as nickel and cobalt that are already in very short supply. Conventional lithium-ion batteries pose a safety threat as well, in case of malfunction or degradation, the battery could heat up rapidly (known as ‘thermal runaway’) and ultimately result in an explosion. Such batteries also have a large environmental impact due to the notoriously difficult processes involved in their recycling. Although the energy-storage industry is evolving rapidly, new, more efficient, and safer battery technologies will be critical for the transition of the shipping industry away from fossil fuels.[30]

Alternative Fuels

Insofar as alternative fuels are concerned, biofuels are already being used as a transitionary low-carbon-alternative to oil. In the long term, zero-carbon fuels will be required to completely decarbonise the shipping sector. In this context, liquid hydrogen (or compressed gas) offers a promising solution due to its high calorific value and zero carbon-content. There are, however, significant challenges associated with commercially-viable production and storage, since hydrogen exists as a liquid only at very low temperatures and very high pressures, and is highly flammable. This issue could potentially be solved by using a precursor (such as ammonia) instead, which may be relatively easier and safer to store and could then be converted to hydrogen at the time of operation. As is the case with battery technologies, vigorous research is being carried out around the world to determine viable solutions to these challenges.

Of course, merely developing a low-carbon fuel will not solve the problem entirely. It will only be the first, albeit critical, step towards large-scale decarbonising of the maritime trade network. The accessibility and scalability of the fuel will determine its practical efficacy. Appropriate infrastructure to store and use the fuel on new and existing ships, and the infrastructure to store and supply that fuel at international and smaller, national ports will have to be established accordingly. Similarly, if the battery storage problem is solved for larger ships and the industry decides to add a certain number of electric ships to existing fleets, then appropriate ‘charging stations’ will have to be installed at ports worldwide. These ‘charging stations’ must themselves be powered by renewable sources of energy in order to make the ships truly ‘carbon-free’.

Implementing the measures mentioned above will require large-scale and long-term cooperation — not only between nations but also between public and private sectors. Developed nations that have the financial and infrastructural wherewithal to innovate and explore zero-carbon technologies must take the lead. In this context, capital investments from the private sector will play a critical role. In an encouraging effort last year, a group of international banks committed to integrate climate change considerations into loan agreements to shipping companies with the idea of incentivising projects that aim to reduce carbon emissions.[31] It must be also ensured, through appropriate mechanisms developed by the IMO, that such technologies are then made accessible to developing and least developed countries.

*********************

About the Authors:

* Dr Pushp Bajaj is an Associate Fellow at the NMF. His current research focusses upon the impact of climate-change upon India’s holistic maritime security. He may be contacted on climatechange2.nmf@gmail.com

** Dr Sameer Guduru is an Associate Fellow at the National Maritime Foundation. His research focusses upon technical issues relevant to India’s maritime domain. He may be contacted at associatefellow3.nmf@gmail.com

*** Mr Akshay Honmane and Ms Priyanka Choudhury are both undergoing their internships (Summer 2020 [Extended]) at the National Maritime Foundation. They can be contacted at akshayhonmane.ah21@gmail.com and priyanka.choudhury13@gmail.com, respectively.

Endnotes

[1] Mark D Zelinka et al, “Causes of Higher Climate Sensitivity in CMIP6 Models”, Geophysical Research Letters 47, No 1, (2020). https://agupubs.onlinelibrary.wiley.com/doi/full/10.1029/2019GL085782

[2] “The Paris Agreement”, United Nations Framework Convention for Climate Change (UNFCCC). https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement

[3] Myles R. Allen et al, “Summary for Policymakers”, in Global Warming of 1.5°C. An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty, eds. V. Masson-Delmotte et al., (Geneva: World Meteorological Organisation, 2018). https://www.ipcc.ch/sr15/chapter/spm/

[4] “International Energy Outlook 2019,” US Energy Information Administration (EIA), (assessed 10 August 2020). https://www.eia.gov/outlooks/aeo/data/browser/#/?id=49-IEO2019&cases=Reference

[5] “IMO Profile – Overview”, International Maritime Organization (IMO). https://business.un.org/en/entities/13

[6] Simon Bullock et al, “Shipping and the Paris climate agreement: a focus on committed emission”, BMC Energy 2, No 5 (2020). https://bmcenergy.biomedcentral.com/articles/10.1186/s42500-020-00015-2

[7] Naya Olmer et al, Greenhouse Gas Emissions from Global Shipping, 2013 – 2015, International Council on Clean Transportation, (Washington DC: 2017).https://theicct.org/sites/default/files/publications/Global-shipping-GHG-emissions-2013-2015_ICCT-Report_17102017_vF.pdf

[8] “International Shipping,” Climate Action Tracker, last modified June 25, 2020. https://climateactiontracker.org/sectors/shipping/

[9] Kalgora, Bomboma and Christian Tshibuyi, “The Financial and Economic Crisis, Its Impacts on the Shipping Industry, Lesson to Learn: The Container Ships Market Analysis,” Open Journal of Social Sciences 04 (January 2016): 38 – 44. https://www.scirp.org/journal/PaperInformation.aspx?PaperID=62786

[10] Ibid

[11] Third IMO GHG Study 2014 – Executive Summary and Final Report, (London: International Maritime Organisation (IMO), (2015). http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Documents/Third%20Greenhouse%20Gas%20Study/GHG3%20Executive%20Summary%20and%20Report.pdf

[12] European Union, “Regulation (EU) 2015/757 of the European Parliament and Council”, Journal of the European Union, (19 May 2015): 55-56. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32015R0757&from=EN

[13] “European Union MRV Regulation”, International Chamber of Shipping (ICS). https://www.ics-shipping.org/docs/default-source/resources/ics-guidance-on-eu-mrv.pdf?sfvrsn=10

[14] Ibid

[15] “Data Collection System for Fuel Oil Consumption of Ships”, International Maritime Organisation (IMO). http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Pages/Data-Collection-System.aspx

[16] Ibid

[17] Third IMO GHG Study 2014 – Executive Summary and Final Report, IMO.

[18] Naya Olmer et al, Greenhouse Gas Emissions from Global Shipping, 2013 – 2015.

[19] “International Convention for the Prevention of Pollution from Ships (MARPOL)”, International Maritime Organisation (IMO). http://www.imo.org/en/About/Conventions/ListOfConventions/Pages/International-Convention-for-the-Prevention-of-Pollution-from-Ships-(MARPOL).aspx

[20] IMO Train the Trainer (TTT) Course on Energy Efficient Ship Operation, (London: International Maritime Organisation, January 2016), 19. http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Documents/Air%20pollution/M2%20EE%20regulations%20and%20guidelines%20final.pdf

[21] Shipping, World Trade and the Reduction of CO2 Emissions, (London: International Chamber of Shipping, 2014). https://www.ics-shipping.org/docs/default-source/resources/policy-tools/shipping-world-trade-and-the-reduction-of-co2-emissionsEE36BCFD2279.pdf?sfvrsn=20

[22] “Why so many shipowners find Panama’s flag convenient”, BBC, 05 August 2014. https://www.bbc.com/news/world-latin-america-28558480.

[23] Marianna Parraga and Elida Moreno, “Panama to withdraw flags from more vessels that violate sanctions”, Reuters, 13 July, 2019. https://in.reuters.com/article/mideast-iran-tanker-panama-exclusive/exclusive-panama-to-withdraw-flags-from-more-vessels-that-violate-sanctions-idINKCN1U72E9

[24] “United Nations Convention on the Law of the Sea”, United Nations, 55-56. https://www.un.org/depts/los/convention_agreements/texts/unclos/unclos_e.pdf

[25] Andrew Murphy, “Planes and ships can’t escape Paris climate commitments”, Transport and Environment, May 4 2018. https://www.transportenvironment.org/newsroom/blog/planes-and-ships-cant-escape-paris-climate-commitments

[26] “Note by the International Maritime Organisation to the UNFCCC Talanoa Dialogue”, International Maritime Organisation (IMO). https://unfccc.int/sites/default/files/resource/250_IMO%20submission_Talanoa%20Dialogue_April%202018.pdf

[27] “Energy Efficiency Measures”, International Maritime Organisation (IMO). http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Pages/Technical-and-Operational-Measures.aspx

[28] “Marine Environment Protection Committee (MEPC) 61st session: 27 September to 1 October 2010”, International Maritime Organisation (IMO). http://www.imo.org/en/MediaCentre/MeetingSummaries/MEPC/Pages/MEPC-61st-Session.aspx

[29] MEPC 1/Circ 794, “On-Shore Power Supply”, International Maritime Organisation (IMO), 09 October 2012. http://www.imo.org/en/OurWork/Environment/PollutionPrevention/AirPollution/Documents/Circ.794.pdf

[30] Daniel Oberhaus, “Want Electric Ships? Build a Better Battery”, Wired, 19 March 2020. https://www.wired.com/story/want-electric-ships-build-a-better-battery/

[31] Michael Parker and Johannah Christensen, “Banks Launch Green Charter to Help Shipping Reduce its Carbon Footprint”, World Economic Forum, 18 June 2019. https://www.weforum.org/agenda/2019/06/how-banks-are-leading-shippings-green-transition

Image Credits: IMO

Image Credits: IMO

Image Credits: The Economic Times

Image Credits: The Economic Times ") Image Credits: Deltamarin Ltd

Image Credits: Deltamarin Ltd

Image Credits: gCaptain

Image Credits: gCaptain

Leave a Reply

Want to join the discussion?Feel free to contribute!